October Update // Starting the Transition to FIRE

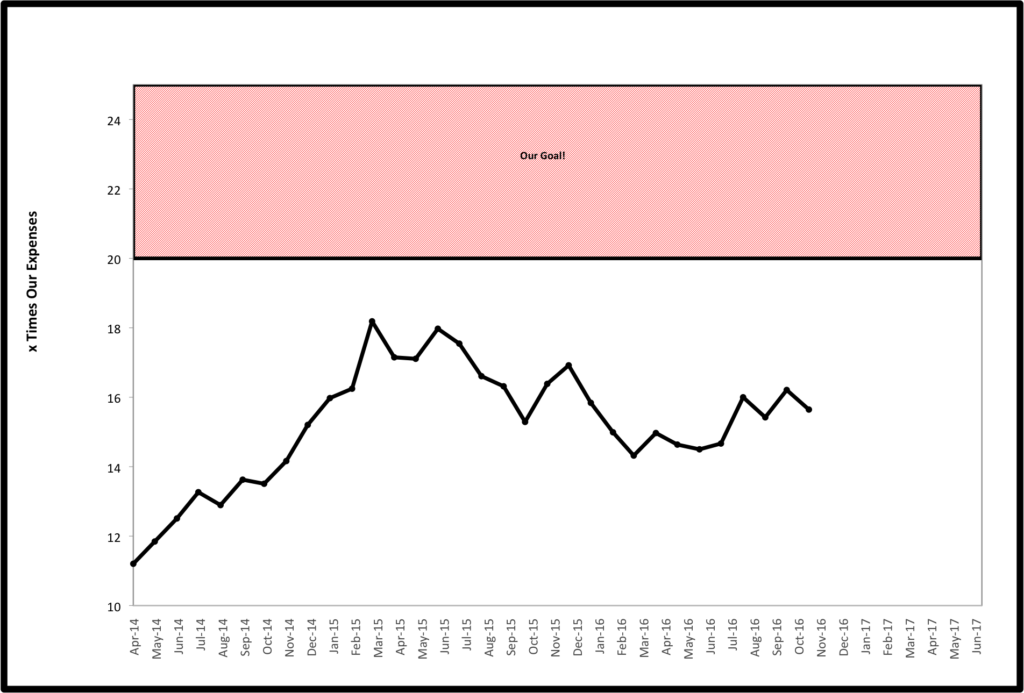

Back On The Roller Coaster

Back On The Roller Coaster

After hitting our high point for the year last month, the graph took a dip this month. On the investment side, nothing was pretty. The only asset class that we hold that went up in value was emerging markets (↑.67%), while everything else we own took a hit, most notably REITs (↓5.70%). Overall our assets were down 1.44% for the month despite upping contributions as year end incentive pay and side-hustle income has been kicking in. On the spending side, we were doing excellent until a couple of big end of month expenses occurred including needing brakes to pass car inspection ($250), needing a repair to the furnace ($275) and deciding to register early for next year’s FinCon conference ($200). That accounted for most of our $1,000 increase in spending from October 2015. Factor it all in and assets as a multiple of our yearly spending dropped from 16.2X to 15.6X.

Starting the Transition

We are now under a year until we plan to start the transition to our ultra-safe early retirement plan. As such, we have started to transition our investing strategy and I made a big career decision this past month.

More Money

On the financial side, we have stopped automatic contributions to Vanguard taxable investment accounts . We are instead starting to stockpile cash. Mrs. EE traditionally likes the security of a cash emergency fund while I generally feel it is a drag on our investments and so our compromise was to always keep about 3-6 months of expenses in savings. We will soon give up the excess cash-flow that comes with having two full-time incomes. We also have uncertainty of expenses with selling our home and likely making a cross country move in the next year or two. We agreed it is time to ramp up cash reserves.

We agreed to accumulate at least one year of expenses in cash by the time I leave full-time employment. We will probably stay at the greater of around 1 year of expenses or up to 5% of our allocation per our written investment/asset allocation plan for as long as we are anticipating having a redundant income stream outside of investments. As much as I traditionally have not liked holding cash, we have agreed (after much discussion) that this is a good place for us to be at this stage in life.

We also are considering changing our written plan to increase our cash reserves to about 3 years of living expenses by the time we plan to live solely off of investments. This was after having a long discussion after reading Darrow Kirkpatrick’s “Can I Retire Yet” book recently. In it, he discusses the average and worst case historic scenarios for markets to recover after downturns. The average time is about three years, making this seem like a prudent amount to hold when we are at the stage where we are worried about spending assets at depressed values. However, we do not see that anywhere in our immediate future so it is not a pressing issue.

Less Letters

I made a decision officially on October 31 as the deadline passed that I will not renew one of my professional credentials. Ten years ago, I became an Orthopedic Certified Specialist (OCS) through the American Board of Physical Therapy Specialties by passing a rigorous written test and documenting that I had met other standards related to education and experience. Earlier this summer, I received a packet to renew the certification as is required every ten years.

As I began skimming through what was required to renew, I realized it would take me hours to round up all of the documentation of work history, continuing education, students I had mentored, and professional publication for the past decade. I then looked at the fee I would have to pay, about $1,500 to renew. I quickly decided that there was really no reason for me to do this, and I didn’t really think about it again for months. I received a second reminder just a few weeks ago that the deadline was approaching.

I don’t know why, but after giving this decision little thought initially, it hit me as the deadline approached that this whole early retirement thing is real. As of next June, I legally have to remove those credentials from any professional documentation and stop writing those letters after my professional signature, where they have gone for the past ten years.

After discussing early retirement endlessly with Mrs. EE and writing this blog for the past two years, this is the first real action I have actually taken to start stepping away from the career that has defined me for the past 15 years. I must confess that I spent a few days second guessing my decision prior to the passing of the deadline.

I certainly do not regret the decision as the certification has little to no value to me at this point in my life. It did mean a lot to me personally at the time I got it. However, it has no bearing on my physical therapy license or ability to practice. I have found the designation is of little marketing value. Like many professional designations after people’s names, most people do not even know what it means. This is true of clients and even other professionals. It is certainly not worth the time and money it would require to retain it.

I can’t quite describe what it is that I am feeling when I think about the decision. I guess it is just a little sign that this whole FIRE thing is real. Despite the amount of thought and effort we’ve put into our planning, the reality is that what we want to do with our lives is quite different than what the vast majority of people do. I guess as it starts to get real, I must confess it is a little scary.

Any interesting changes in your plans as you work towards FIRE? For those of you getting close, are you changing anything with investment portfolios or making any other big changes? How much cash do you hold? Anyone else get those butterflies when you make big changes/decisions, even when you are sure they are the right decision? What do you find scary about making the transition to FIRE? Share your thoughts below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

I’ve thought about certifications to become a “professional geologist”, but like an engineer stamp, it requires passing 2 days worth of tests, documenting work history, 5 freaking references… Yet, I haven’t seen any upside to having those letters at the end of my name. I haven’t done it and won’t, especially now.

As far as cash goes, I think we’ll keep a couple of years worth of cash on hand, which is way more than we usually keep around. I’m a fan of a good cash stockpile, but Mrs. SSC sees it as a depreciating asset. Our previous emergency fund was only ~$10k in cash buoyed upward to that amount only by my constant whining. 🙂

The only other, “oh crap, this is getting real” moment I had was talking with a financial advisor, but asking about early 401k withdrawal strategies, ways to diversify beyond bonds, ways to generate income beyond dividends, and more typical retirement questions. It was actually very useful and informative, I know, shocking right? 🙂 The advisor was a free 1 hr session provided by work, at work since we switched from Vanguard to Voya this year.

Our cash consensus was also a result of a spouse’s whining, but I’m not so bold as you to say it publicly, or did I just say it accidentally?;)

As critical as I am of financial advisors, I also just tonight had a very informative and helpful discussion with a CFP from Vanguard who is working with my parents and I to transition over their investments. I used it as an opportunity to pick her brain and learned and clarified a good bit about tax planning and WD strategies.

I can imagine how hard it is letting go of that huge part of your identity, no matter how symbolic or unnecessary it may be at this point! When you’ve devoted a significant number of years to that career, it’s not easy to transition instantly out of it. Great that you’re confident in your early retirement plan and goals so you know you can let it go. Keep it up and we’ll continue to follow your journey to see when you make the big leap!

Thanks for the consistent feedback and encouragement. It is appreciated!

Thx for sharing the thoughts that go into early retirement planning in the last mile. We are far away, yet it is on my mind. Especially the topics on life style changes prior to FIRE are also great to read.

So, I am quite exicited to be able to follow a family that is below the target to make a major lifestyle change already!

On our side, I am consideering a month of parental leave in the summer to be with the family. And the moce from a corporate to a startup alos ment less salary…

Thanks AT. I think that the leave and lower paying jobs are good trade offs for time with the kids now. Our philosophy is that kids are only young once and your health is not guaranteed. You can always make more money later and traditional retirement is not nearly as appealing as improving lifestyle sooner on our eyes.

Like you, I am a PT pursuing FIRE. Very excited about the progress you’re making. You will likely meet that goal before me!

Also, similarly, I hold the OCS credential. Though, I’m the other end of the timeline - I only this year attained mine. This comes after almost 10 years in practice!

Where we differ is our pathways to Fi independence. I am utilizing real estate. This month will be huge as I make a leap into commercial real estate! This deal literally fell into my lap and looks to be the perfect way to start in commercial. It is a mobile home park, so no dwellings, just land parcels. Literally zero maintenance and repairs. Plus, with two young children, a minimally time- and resource-intensive investment is paramount. This one should cashflow at least $900 monthly (potential for $1200!). Saying I’m thrilled is an understatement!

Congrats on the OCS and the successful real estate investing. RE investing is a budding interest of mine and I hope you’ll continue to share your experiences as you go.

I don’t blame you for dropping the letters. The cost in terms of money and time to maintain so many certifications and credentials can be oh, so onerous in the health professions.

The “cash cushion” question is an interesting one. Just like you don’t like a large emergency fund because it’s money on the sidelines, the cash cushion is more or less the same thing.

Early Retirement Now did a detailed analysis that I think you will find enlightening: https://earlyretirementnow.com/2016/10/26/cash-management-in-early-retirement/

Cheers!

-PoF

Agree about the cost and time to gain certifications. One of the things that frustrates me most about the health care industry is that there is no incentive to gain more education or expertise or to even do a good job. Not sure exactly how MD reimbursement works, but with PT we bill codes based on service provided and time taken to provide it. Therefore if you have a lower cost PT assistant take 30 minutes and provide ineffective treatment, you are paid more than having a PT provide effective treatment for 15 minutes. The whole system is a bit maddening to me!

Appreciate the link and I’ll share with Mrs EE. This is very intuitive to me and she is much more emotional with $ decisions. I think this is due to our different family/financial backgrounds that we each bring to the table. The whole idea of data based vs. behavioral based decision making is what I find so interesting about personal finance.

Thanks again for the great comment and insights.

Gosh that’s got to be such an awesome but scary feeling at the same time. Removing that “safety” net has got to make it feel real. Congrats on knowing what makes financial sense and sticking to your guns.

Thanks for the encouragement!