April Upate

Plodding Along

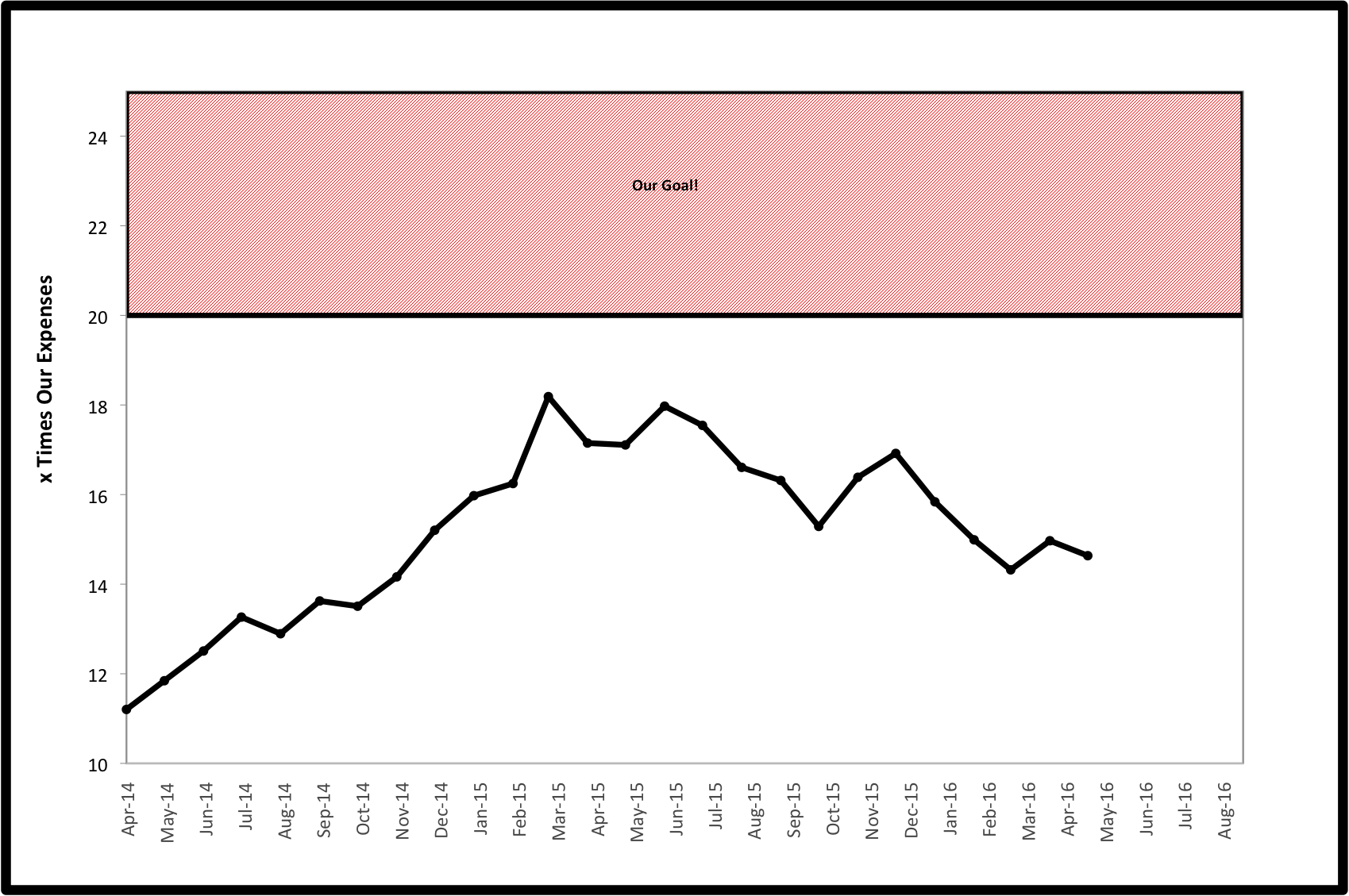

Assets went up 1.44% from last month due to a combination of continued contributions with some small market gains. However, our spending was again up, pushing our average monthly spending up by about $170. Factoring it all in, our assets were down from 15.0 to 14.6X our monthly expenses. More on our spending below.

The Final Countdown!

We are officially one year away from beginning our transition to our early retirement. We have actually been in transition for the past 3.5 years when we had little EE. Since then, Mrs. EE left the full-time work force and has been working 30 hours/week. At the same time, I gave up a portion of my workload and went from a frantic pace to a normal 40 hour work week while also burning through a bunch of vacation time. However, we still feel consistently far too busy and are ready to take much more drastic next steps.

The first big step will happen in one year. I plan to leave my job by the end of next April. My goal, even before I had any idea if it was possible, was to retire by age 40. Next May, I will turn 41. The time has come to proverbially shit or get off the pot! Over the next year, we will be shifting our focus in life and in writings for the blog away from our original focus on building assets, investing and general financial education to the specific questions and challenges we will face during this transition.

As always we encourage any feedback and welcome the bad as well as the good. Over the past 2 years since starting the blog, we have been sporadic in our writing and even worse with our marketing. Despite this, we seem to have developed an awesome core group of regular readers, some already FI and others at various stages of the journey with us who are very knowledgeable. We are grateful for all that we continue to learn from your feedback.

Our Flawed System

We have gotten a good bit of positive feedback regarding our system of tracking our progress towards FI. To recap, we update our investment asset values each month. This includes all retirement and non-retirement accounts and cash savings. We track all expenses each month and keep a rolling average of our annual spending. For example, our spending for this April kicked out our spending from April 2015 as we average the most recent year. We then present our progress as a multiple of assets X annual spending. Using the assumptions of a 4% withdrawal rate, you are financially independent when investments reach 25X annual expenses.

We think that tracking progress in this way is great when starting out for two reasons. First, when starting out with a high savings rate and a low asset balance, your new savings will be the dominant driving force in your asset gains. Thus, you will see consistent gains in your asset value in all but the most drastic market downturns. This positive feedback loop is very encouraging and motivating. Second, this method forces you to focus on your spending. This is vital to those who want to achieve FI quickly. It is far easier to cut $1,000 of annual spending than it is to save $25,000, even for very high wage earners. Tracking expenses in this way makes this very apparent.

We have discovered two problems with this system as we approach our FI number which maxed out at over 18X and currently sits at 14.6X our spending. They are the opposite sides of the coin as to why this system is so good.

We have previously discussed the concept of crossing a line, where your investment returns far outweigh anything that you do with saving. This is definitely a good thing as it is a sign that you have accumulated substantial assets. However, it is challenging psychologically. For example if you have $50,000 and add $5,000/month, you are seeing a 10% return for the month even in a flat market. However, if you have $500,000 and add $5,000/month you have only a 1% improvement in a flat market. In months where the markets are up or down by only 2%, it becomes very apparent that you have little control over asset value. Market forces now have much more influence than you do. This can be challenging psychologically as it can feel that you are wasting your time by continuing to save, when in reality saving is still very important as you are accumulating substantial amounts of shares over time.

Also, our spending has a disproportionate effect on our number. While this is good to be aware of, it also can lead to false assumptions. The 4% rule is based on having constant expenses, adjusting only for inflation annually. This is simply not how people live, especially those retiring very early and going through different seasons of life. Looking at our numbers, it looks like we have taken major steps backward over the past year, when in fact we feel very good about our direction. Despite an overall relatively flat market (with lots of short upturns and drops), we’ve seen a 6-figure increase in our asset values.

Our philosophy is that we don’t have to have the assets to support the living expenses that we have during our working years. We need to be able to support the expenses that we will have in our retirement. These are potentially two very different things and we each have to make an accurate assessment of whether our spending will remain constant, increase or decrease after we quit working. We are consciously choosing to spend a bit more now, knowing that we would not be able to sustain that level of spending on our current assets.

Where Are We Spending More Money?

Tracking our expenses allows us to see where our increased spending over the past year has been going. We are able to divide it into 3 categories.

- Health Care Expenses: Part of this is the traditional sense in which people think, aka health insurance. My contributions to my work provided insurance plan have increased by $200/month. At the same time we are now responsible for higher deductibles. This is actually not a terrible thing as one of the things that has us hanging on to full-time employment is the idea of having health care provided by my employer. Now that we are paying a substantial share of these costs anyway, it makes it less scary to leave my job. Assuming ACA subsidies stay the same (a scary and potentially dangerous assumption), we won’t pay all that much more having to buy our own health insurance. The other portion of these health related expenses is that we continue to experiment with a more organic, whole food diet and the use of supplements as first discussed here. We plan on this being a permanent change as well to some degree. However, we are starting to get a little better at simplifying and prioritizing. As we get more efficient with shopping and designing our menu, I think we can reduce what we are currently spending. All in all though, I don’t see us ever going back to cheaper health insurance costs or the lower cost diet we formerly ate so we will simply have to figure out a way to cover these expenses.

- Travel: We have decided that we are not going to worry too much about what we spend on travel while still working. If we want to fly across the country to ski for a weekend, we feel it is worth it. If we want to stay in a hotel when traveling with little EE rather than camp for improved comfort, we will. While we are still working, we realize that we don’t have a lot of flexibility in our schedules and we are living in a place with poor proximity to good skiing, climbing and hiking. Therefore, we need to pay to play, often premium prices. When we retire, we plan to reverse our current living situation. We will build our lives around living close to the things we want to do and travel to our current home town to visit with family. We will be able to play much more for much less cost. We will be able to travel for longer periods of time and stay for far lower costs. We also decided to invest some time to learn about travel hacking with the Travel Miles 101 course. As we get better with these techniques and have more flexible schedules, we will be able to travel much more for much less cost. All in all, I don’t worry about this being spending that we have to sustain long-term and feel that it is far better use of our money to enjoy life now instead of worrying if we can save a few thousand dollars a year more. However, this spending makes our FI numbers look really bad as every $1,000 we spend is the equivalent to $25,000 we should have saved by our formula.

- Home Repairs/Maintenance: We made a final decision that we will be putting our home on the market and have met with a realtor. This means doing a number of cosmetic projects including landscaping, fencing, painting, power-washing, etc. We feel that it is a far better investment of our time and money to pay to have these things done for us when time is at a premium. We would much rather use our time on things more important to us right now such as our marriage, little EE, developing side hustles that will provide long-term ongoing income, our hobbies, friends, and charitable endeavors. While this is a significant expense now, these projects are in no way annual expenses. In the long run we will spend far less on our overall housing costs as we are looking to significantly downsize as part of our early retirement plans. Therefore, we are not really worried about sustaining this spending. However, like the travel expenses, this current spending makes our numbers look substantailly worse.

So that’s where we are with our spending and why we seem to have hit a wall in our progress towards FI, even as our asset value consistently grows.

So what do you think? Are we being realistic with our assessments and smart with our moderation in saving as we come down the home stretch to FIRE? Are we just trying to justify reckless spending which is a sign that we are getting soft and lazy? Are we setting ourselves up for hard times if we have to cut back spending later? Share your thoughts below. We appreciate you honest feedback!

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

Hi

This is fantastic. I’m so glad I found your blog. The 25x multiple so assuming a 4% drawdown rate I find a highly credible methodology. I saw some figures here in the UK from Fisher Investments about pension “pots” and their chances of lasting out till death and with the right asset ratio 4% appeared optimum.

The sale of your house is an interesting one. Much of my wealth sits in these 4 walls and the step of selling the family home is a big psychological one for me. I’m also torn between turning it into an income - renting it out - and realising the cash with the geographical freedom and flexibility that would afford me.

Richard,

Just to clarify, while we would consider home equity as part of our net worth, we don’t count it as part of our assets for retirement. We feel that it is a consumption item that drives our spending and it doesn’t produce any income on a monthly basis. I do share your ideas of changing that around and having less money tied up in our primary residence when it could be converted into a source of income.

Thanks for the comment.

EE

The spending in things you love doing now is healthy if it is kept in balance. Your post resonated with me a lot. We have gone from a quite “spendy” couple to a savings rate that we could never have imagined a year ago. It is easy to be laser focused on a goal and completely forget to live now. That is a mistake many pursuing FI with a passion make.

Take that ski trip. Enjoy it. And like skiing, make sure you find the balance.

I agree that we got overly focused on savings rate there for awhile. To be clear, we are still saving well over 50% of our income including maxing out 2 401(k)’s, two Roth IRA’s, saving the remainder of my salary in taxable accounts and saving all of the money from our side hustles to front-load little EE’s college savings. What we’re talking about is not depriving ourselves of vacation or spending our little limited time to DIY home improvement projects, when saving a bit more will have a small impact on our long term retirement plans and quality of life, while spending more now will greatly improve our quality of life.

I think your steps forward are awesome! (Also I think the TravelMiles101 course is amazing! - it helped pay for all the hotels in London/Paris for our big trip next month!) And I’ve always loved the way you track your progress… but I do see the downfalls now that your investments are larger.

Agree 150% on the course being amazing. It saved me so much time and so many mistakes that we were making and would have continued to make trying to figure it out on our own.

We will definitely continue to report our numbers in the same way, regardless of how good or bad they may look. It will be interesting if we are projecting things correctly. If so, our numbers will look much better in retirement, even as we transition from saving up to spending down our assets.

We have a similar mindset in that you have to find balance, otherwise it will feel like a chore and it will be easier to get disillusioned with the whole thing. So we will do things that may seem extravagant, while we are working and have the felxibility to do that, and we will do things like hire someone to do some work for us because of the value of our time versus money. I’d rather have time currently and other people would rather have money, so I see it as a fair trade. 🙂

As far as having to pay to play - I hear you there. No skiing down here in the Gulf States, and even to get to some decent hiking (beyond the Hill Country) it’s a good 10 hr drive or more, or you fly. Enjoy it now while you can.

As far as tracking, your way seems to work for you and is defendable, so that’s my 2 cents on it. We have a “yearly spend number we want to target, and our assumptions are all based off of maintaining that number yearly, and using 4% withdrawal rate. That’s assuming no side income, and no other decrease in spending. We always analyze, what would it look like at 3% or 5% or if we had $12k / year in income, and it just helps, hurts, or does nothing to the end game. It does make me feel more comfortable with it though. If your system works for you guys, then keep it and nuts to everyone else. 🙂

From following your blog, I think we’re in the same boat as you in that we got a little over focused on getting to FIRE. We took something that we were already good at, having a high savings rate, and turning into an unnecessarily stressful thing in trying to have an optimal savings rate and path to FIRE. I love to see that Mrs. SSC is taking the less stressful teaching position and it is similar to what we did when Mrs. EE never went back to FT work and now we are relaxing even a bit more. At the end of the day, it doesn’t matter if you save an extra 5-10% of your income if you completely burn yourself out on the way. As you are learning in fitness and finance, you can’t run a marathon at the same pace as a sprint!

Congratulations! Striking the right balance for your own personal situation is important to keep in mind. It’s got to be sustainable, for you. We left our corporate jobs at 51, after kind of backing into the realization that our high savings rate over the years had magically given us that option 🙂 While working, we did feel free to enjoy the experiences we really valued, and that hasn’t changed. After almost 4 years since leaving our jobs, we’re still selectively doing the things we really want to do (plus enjoying having time to read all the great blogs like yours, and other resources to help guide us through). “Everything in moderation”, if it adds value to your life. And, thanks for the tip about the travel class ~ we’ll check that out!

ST,

Thank you for the positive feedback. We always love to hear from people “on the other side”. Definitely check out the TM101 course, it is really a great resource!

Cheers!

EE

The system you have seems to make sens to me. I especially like the fact that Ms. EE spends already ow more time at home. Since a few years, my wife also works less. It indeed means less income and less saving/investing. We are ok to do this, as we want to life the life we want not only pot FIRE, we also want it now!

In that mindset, going on a ski trip is worth it. As long as it happens in cash, not with credit card debt.

What if your method to calculate the progress would exclude the one off charges of the house maintenance? I would keep the travel tough.

We honestly are really bad budgeters/trackers and don’t really care to complicate things further by taking things out. We like just logging all our spending for simplicity and we’re fine just giving it the eyeball test to see where our money is going.

As for finding more balance, I think it is a good idea for everyone to keep in mind. I can see going all out for a while and then just being done for single people or DINK couples. For those with kids, I personally think it is not very smart to put everything off for the future when you have little ones b/c time with your kids is so valuable, goes by so fast and you only get one shot.

Gogogogogogogo! I think you are going to be just fine. So looking forward to you joining me in FIRE.

Not as much as I am my friend 😉

Wow, you are so close. I’ve chosen to work part time even though I’m the breadwinner to have more time with our kids. Agree on the travel - you can put it off, need to get a good balance. Where do you plan on moving to? Somewhere smaller?

We plan on moving somewhere to the mountain west. We would like to live in a smaller town, with a reasonable cost of living very close to mountains/skiing. We have not made a final decision yet but a couple of options we would seriously consider are Driggs, ID, Ogden, UT and a few locations in CO.

I’m very excited for all of you, it is getting close. I would like to suggest some ideas for “passive income” while you’re independent. I realize that rental property may have risks, but I find it far more profitable than stocks/banks. Also, the tax write offs make it even better. Best of luck in your endeavors and wish you all the best on your goal of FI.

Hi Ed,

We’re definitely on the same page there. We love the passive nature of our current approach while working, but agree 100% with the idea of diversifying into real estate which has more potential upside and more stable returns once we have some time to devote to learning to do it correctly. Appreciate your feedback. Your $.02 are always welcome here.

Cheers!

We totally feel your pain on the markets having all the control… but that’s how we know we’re doing it right, isn’t it? 😉 But yeah, we can have a month of saving some monster amount and still end up flat… flipside, though, is that we can have a lackluster savings month that still looks big on paper. Oh well. 🙂

On the health eating, I did supplements for a while, too, but ultimately found that it was eliminating the unhealthy foods and focusing on the good ones that made the difference. I was happy to stop purchasing all that stuff!

And selling your house! What are you guys going to do next? Are you going to buy a smaller home where you are? Rent? Move west? Go #vanlife? 😉 I’m so curious! Good luck with the sale!

Totally agree that the big swings are a good thing b/c it means you have substantial assets. Still it makes it hard to keep “punching the clock” to collect a paycheck that then gets applied to investments and doesn’t even “seem” to make a difference. (I know it absolutely does over time, I just have to keep reminding myself.)

I currently am not using any supplements, but Mrs. EE is still experimenting with a few including probiotics, Vit D, calcium and omega 3’s. She started on about 15 and is weaning down and hopefully will get to that point as well. We are going to do a follow up post at some point, possibly wait a full year, but she is feeling much better on the new diet.

Definitely no #vanlife with a toddler. I’m adventurous and all, but…. We really aren’t sure what we want to do or where we want to be long term. We are leaning towards renting a place for a year or two to vet an area and if we like, buy there and if not move on and do it again.

There was just a good study that came out about probiotics, basically saying they don’t do much for most people. Not to be a parade rainer, but to save you $$! http://www.huffingtonpost.co.uk/entry/no-evidence-probiotic-drinks-work-study-suggests_uk_5731b954e4b0e6da49a6d354

And haha, I was joking about van life. 🙂 I love your rental plan. Do you have any target areas in mind? I assume you need to stay put in your area for at least your last year, but maybe you are hatching plans to find a job elsewhere…

Driggs, ID on the back side of the Tetons is currently looking like our top choice. Also like Ogden, UT and have several locations in CO are still considerations. Definitely haven’t ruled out doing some continued part-time professional work in the future if the ideal setting and opportunity arose, but that is definitely not a factor in our choice. If one of us keeps doing regular work it would be Mrs. EE who still really loves her job and already has ability to work from home, part-time and is location independent.

Congrats on being so close to an early retirement. To be able to do this at such a young age is evidence that you’ve been prudent with your finances for a while. Anyone who can call it quits before the age of 50 has done a great job in my book.

Thanks for the positive feedback and encouragement. We’ve definitely always been good savers, but have made a ton of mistakes along the way, especially with investing. It goes to show that you definitely don’t have to be perfect as long as you get most of the big things right.