July Update

Well That Looks Better

Well That Looks Better

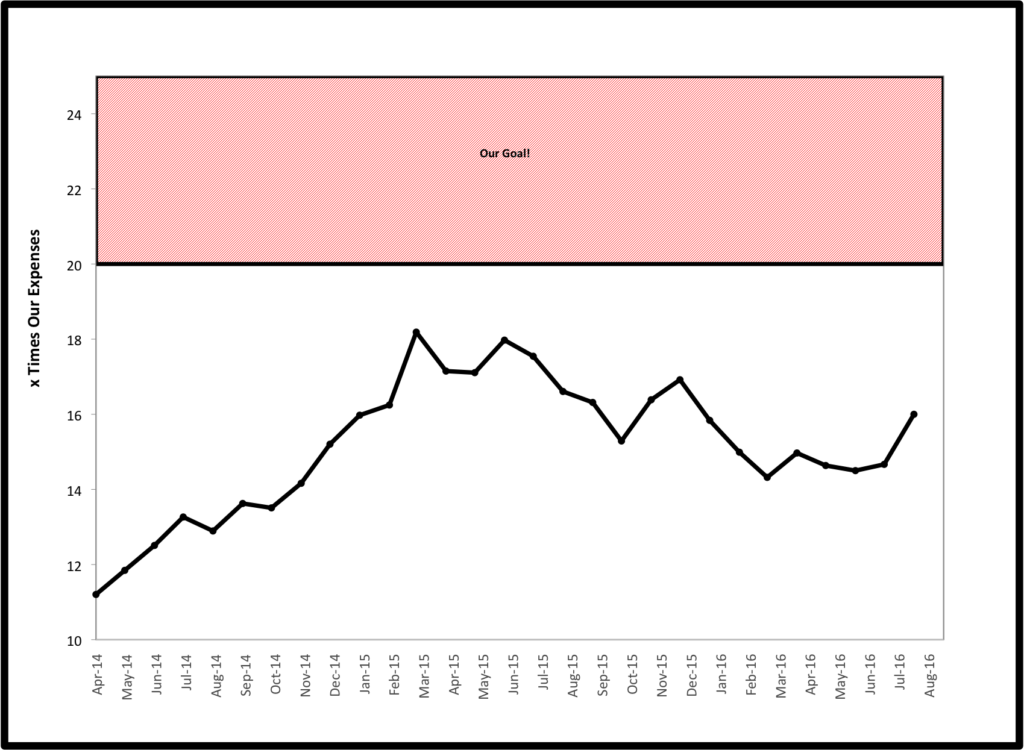

After seeing our graph sputtering along for awhile, it is nice to see the big jump upward. Our assets as a multiple of our spending increased from 14.7X to 16.0X over the past month. This was a phenomenon of two things we have been writing about recently.

On the spending side we have had a few house projects going on over the past year as we have an eye to getting the house ready to sell. Our spending was actually a bit higher than a normal month this past July. However, in our rolling 12 month average, we kicked out last July when we spent over $7,000 with a large portion of that going to a major landscaping project. Thus, our average spending went down by nearly 4% by getting this one time large expenditure “off the books”.

On the investment side, again we did nothing special except sit back and watch the markets take off. Our investments were up 4.34% for the month. Because of the size of our portfolio, market forces have much more control over our direction than anything we are doing.

Just as we wrote over recent months that we were not getting overly concerned when the graph was looking kind of bleak, we are not getting overly excited with the current spike. Instead, we continue to focus on our processes of automated investing and slowly systematically simplifying life. Over time these processes are bound to continue to push our numbers higher as we work towards FI.

If You Want to Change the World, Start at Home

Each month in this space we discuss things that we are learning, thinking about, or problems we are working through as we “eat the financial elephant”. This month I am very excited to share that the financial issue that is dominating my time and thoughts is not focused on us, but helping out my parents.

I have written extensively about our lousy experience with a financial adviser. Not only did we pay far more in fees than we realized, in the process we were receiving horrible advice.

I originally was embarrassed by how naive and trusting we were, and in retrospect how stupid we had been with very large (at least for us) amounts of money. My initial inclination was to bury my head in the sand.

As I began reading and studying the topic, I found that the advice we received was pretty typical to what is available to those starting out with low net worth. As I shared my interest in this topic with others who were trying to improve their finances, I found most were making the same mistakes and receiving very similar advice from a variety of different advisors and firms. I started this blog with what was possibly a slightly overambitious goal of changing the entire financial industry.

Slowly, I did turn different family, friends, and a co-worker onto becoming more financially literate and taking control of their investments. I recommended sources of information. I helped a few move their investments, save substantial money, and simplify portfolios. I got my sister-in-law out of a variable annuity she had been talked into when rolling over a retirement account after switching jobs last year. Mrs. EE and I both even managed to change our work retirement plans substantially.

However, my parents, who were using the same adviser we were, receiving similar advice to what we were, and among the first people we talked to about all of this, remained reluctant to make changes or even explore the idea. They thought that learning about investing at this stage in life was too complicated. After working with the same investment firm for decades, they had no idea what they were invested in or why. They had no idea what fees they were paying each year and no concept of the tax implications of their investments. They did not think they could manage an investment portfolio for themselves. Am I the only one who thinks this complexity and lack of transparency could be by design to the benefit of the costly advisors?

I was a bit surprised and very excited when they recently asked me to help them with taking control of their investments. I reviewed a few things with them and offered to help. We are now in the process of moving their investments from a notoriously high fee firm to Vanguard, saving them about 80% of their annual investment costs while putting them in more favorable investments and reducing the riskiness of their portfolio.

Beyond simply saving money, this process has opened up some interesting conversations between us. As much as possible with respect to their privacy, I hope to share some of the ideas about how they can use their newfound understanding of their investments to improve their lifestyle and do things that they truly value with their money, rather than having their money simply siphoned off to some massive corporation. Hopefully sharing this experience will also provide an opening on the blog for some interesting conversation addressing our society’s taboo about mixing family and money.

I still would love to change the financial industry. While that is a pretty overwhelming challenge, kind of like eating an elephant, I continue to take pride in the bite size wins. I have no idea if I can make any noticeable financial impact on the world. I do feel pretty good on progress made within my own little section of the world.

Are you riding the wave of the markets up this month? Do you mix family and money to help others? Share any stories about strategies and techniques that have worked, and more importantly what has not!

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

That’s a great story about helping out family with finances. I’ve ahd a recent win here at work, in talking about finances and it making a difference. One of my co-workers wanted to invest outside of work related investments but didn’t know how or why.

I sent her some links, but mainly pushed if she was tracking her spending, because then she’d know how much she could invest. Not only did she start tracking her spending but she realized letting her husband handle most of the finances, they’d racked up about $7k in revolving credit card debt.

She put together a debt snowball plan and has almost paid that down now. Plus, she set up an investment account and is researching what assets/funds/etc… she wants to invest in when she gets that debt pay down money freed up.

It was awesome seeing such a big change with what seemed like a simple conversation! My advice is talk, talk, and talk some more because you never know who is paying attention and how it may affect them.

Awesome! I agree with the talk, talk, talk advice but with the caveat of more answer, answer, answer and be an open book to those that want to learn, but not pushing ideas or beliefs on others who aren’t ready to hear it. My approach is to tell people about our blog and offer to help with anything they don’t understand. It has allowed me to help people who want it and also has given me a nice feedback loop about the clarity (or more often lack there of in my writing).

Most of the stuff that it takes to become financially independent is very simple, but it requires a desire to do it first. Knowledge without desire is kind of worthless IMO.

That’s a SWEET WIN!!! I’m always here to lend a hand, voice, and ear for friends and family with respect to handling finances… It amazes me how advisors and so forth just try to cover the costs of their services in the details… I understand they are trying to make a living to feed their family as well..

However, like many industries the times have changed a lot.. ROBO advisors are the next wave in finance for those who chose not to manager their own Financial House.. Human advisors are simply an artifact of the way the system used to be…. and for the most part expensive for no value add… other than helping them buy a boat.

My portfolio has grown so much in the last month I can’t keep up with it… It’s awesome.. but I pay attention to the process not the size of it… When I process is working… the size and scale of the actual portfolio will soon follow. I have a lot of friends and coworkers who still… “Have a guy”… it’s something they are willing to pay for I guess… But I also openly talk about how much money I have and how little I pay in fees and expenses which contributes to my compounding and how it has become a freight train that I can’t stop… (that usually will peak someone’s interest) I mean having more money then you can figure out what to do with it is not usually the problem most people have.

Cheers!

Nice to see a little bit of a turn around in your charts. It can get discouraging at times.. but its all about believing in the process and you do! Time will solve all those little issues you are working thru.

Thanks for the positive feedback Tim. Agree win most of your sentiments, but funny that you mention robo advisers being the new wave. I don’t agree with that and have a full post on it coming next Monday. Curious to get your thoughts once it is out.

Looking good. Gogogogogogogo!

🙂

I was so glad that my month saw gains, even as I am trying to learn to appreciate and roll with volatility. I have not been able to help out any family lately, but a friend came on some hard times and I was able to help him some. Small, but decent. Which is all I can hope to be.