September Update

Back At The Blog

It’s been a while since our last post. Since then, I’ve received several nice comments from regular readers as well as being contacted by some people who I didn’t know were readers asking if we had given up the blog. We have not.

Over the summer the blog was starting to take off. We were having a hard time taking care of all that goes with trying to maintain and grow it while still squeezing in all of the activities that we wanted to do. I decided to step away from writing for a bit to re-prioritize life.

Summer has been great. We’ve spent many days in and on the water with little EE. Mrs. EE and I have found the time to get out of the gym and back out into nature climbing and hiking. As life has gotten back to normal, I’ve again got the itch to start writing so here we go.

Before we get started, I want to say that I greatly appreciate the feedback. I guess it feels good to be missed? It is extremely rewarding to know that people are gaining value using the blog to improve their finances and their lives. If you haven’t already done so, introduce yourself in the comments or if you’re a more private person shoot us an e-mail at our contact page. We love to know that you’re reading and learning with us.

Little Progress Apparent

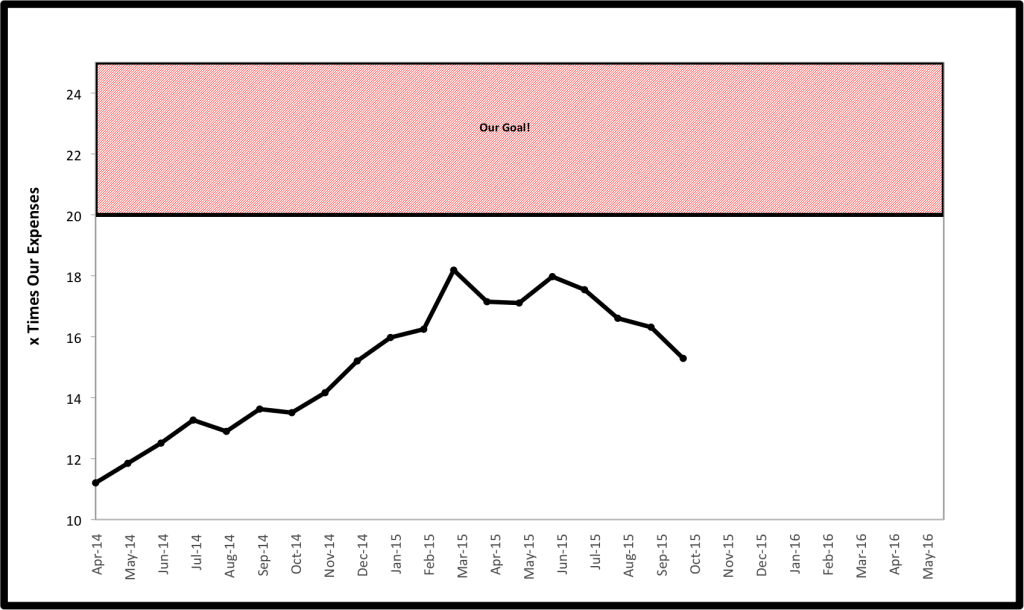

Due to down (and up and back down) markets, our chart continues to look worse. Our investments are now 15.3 times our expenses as the graph continues to drift downward.

Our investment values are down around $40K since May despite continuing to pour my whole salary and a significant amount of Mrs. EE’s into our accounts.

Our way of tracking spending, using a rolling 12 month average of our expenses makes things look even a bit worse. However, much of our bloated spending has been on finishing up a major home project that should more than pay for itself in increased home value. We also payed all of our annual insurance this past month (more on that below) making the numbers look even larger. As those numbers work themselves out and those expenses come off of the books, the numbers will look much better.

Another Big Bite!

Our blog, like many other blogs on early retirement, focuses on building wealth. After all, to this point that is our story.

However, as we accumulate wealth we know that we need to start switching our focus from asset accumulation to asset protection. One real threat that we face living in these litigious times is the threat of liability. We are always hesitant to buy any insurance coverage. We hate buying something that we most likely won’t use. We know that buying insurance is, in sum, a losing bet. However, we also know that it is crazy to be penny wise and pound foolish.

So we decided to explore an umbrella liability policy. The cost of about $150/year for an additional $1M of liability protection is about what we expected. However, we were pleasantly surprised to find out that by bundling the policy with our car and homeowners insurance (which we have been too lazy to shop for the past 2 years) we could save over $500. Therefore, in sum we added $1M liability coverage while paying in total $350 less per year for insurance than we did last year.

Two lessons learned here.

- Umbrella policies can add significant financial protection at a very affordable cost.

- ALWAYS shop your car and homeowner’s insurance policy annually for substantial savings.

Fall Harvest?

For the first time in the couple of years since we’ve been managing our own finances, we have seen substantial drops in the value of some of our investments. This presents the opportunity to do some tax loss harvesting. As we have sat down and looked at the numbers, we question whether it is time to lock in some investment losses for tax benefits. If you are not familiar with tax loss harvesting here are two excellent resources that will give a good introduction to the benefits and some of the rules and potential complications when carrying this out.

As we have examined our own options, we have seen substantial drops in our taxable accounts. We decided not to take advantage of the losses in our domestic funds because they are relatively small and the would interfere with buying the same funds in my retirement account. We did have bigger losses with our international funds and we could sell them to lock in losses of over $10,000 which would cancel out most of the gains we have taken this year on the old actively managed funds we have already sold off. This would leave us with a smaller tax bill. However, we’re not sure it is worth the headache yet. Here are a few issues we are dealing with.

We would have to sell off over $100k of assets to lock in about $10k loss. This would negate taxes on $10k of other gain which is taxed at 15% saving us $1,500 real dollars on the tax bill. While the savings is nice, that is a big shift in our investments.

When selling the investments to lock in the loss, you can’t simply re-buy the same investment until waiting 30 days due to “the wash rule“. This means to get the tax benefit of the loss, we would have to sit out of the market for 31 days or shift our investments to a “substantially different” investment.

If the new investment goes down further in the next month, we could resell it and lock in even more losses and then buy back the original investment which would be ideal. However, if the investments go up in value in that month we have to have an investment option we would be happy to stick with for the long haul or be forced to take on short term capital gains taxes to sell off the new investments.

We have considered multiple options and this is what we think is best at this point. We could shift our investment strategy from slice and dice (we currently own a European, Pacific Rim and Emerging Markets fund for the rebalancing benefits) and simplify by buying the Vanguard total international fund, which holds the same securities in one fund in different proportions. However, this represents a shift in a substantial portion of our long term policy that we developed based on what we felt most comfortable with, for a short term $1,500 gain.

So far, we have elected to stand pat versus the complexity of making any changes to our investments. However, we continue to watch and consider and I am curious to hear what other DIY investors are doing or have done.

As with all things we remind you that we are not investment or tax professionals. We are discussing our own ideas for dealing with our own finances. We would love to hear how other readers are dealing with the issues of risk management and tax management to compare notes and continue to learn. Contribute your ideas below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

So glad you’re back. I enjoy reading your blog and following your progress. Best of luck on continued success. -Ed

Thanks for the positive feedback Ed!

Nice to hear from you! Glad to know that’s you’re all doing well. I’ll chime in as someone who has missed your voice here 🙂

Ugh… The market ride. We’ve also passed on the tax loss harvesting, at least for now, for basically the reasons you cited. And good to hear your perspective on umbrella insurance. We’ve been considering it, too. We are generally less insurance averse, but certainly don’t need to be adding expenses as we get closer to retirement. I’ll explore the bundling question. Thanks for that tip!

Thanks for the kind words. Not sure what we’ll ultimately do with the harvesting but I don’t think it is a big make or break decision.

We have been throwing around the idea of liability insurance for a year or so now…. but hate the idea of spending more money on another type of insurance. Your idea of looking into bundling it is a great idea!

I’m glad you are back! We have gone throw ebbs and flows with our posts too… living life is the most important way to spend our time!

Thanks for the feedback. I’ve been following you guys as you work through the layoff scenarios. Best to you.

So glad to see you back! And plus-one on the umbrella coverage. I have some as well (between rental property/auto/etc.) and it hardly added anything to the cost but left me feeling super covered. You are spot on by viewing this as a penny-wise-pound-foolish decision. We all hate to pay for insurance, but imagine not having it when you really need it?! One serious event could wipe out your whole net worth if you aren’t covered. Yikes.

Thanks for the feedback MarciaB. Our thoughts exactly and glad we pulled the trigger on that one (especially since it forced us to look at our other insurance and overall save money while substantially increasing our protection).

Welcome back! Glad you were able to get out and enjoy life a bit. I was in the same boat as you when it came to umbrella insurance. I was surprised when we got it quoted out after bundling and it really wasn’t costing us anymore even though we had more protection so it was a no-brainer to us.

Better coverage, less cost. Yes please! Wouldn’t it be nice if all decisions were that easy?

Great to see you back!!! Also great news to hear from someone else that had a portfolio that has been getting clobbered… I had a goal to invest $100K this year and while I’m on track with that… My overall networth has been mostly stagnant to losing value since most of my investments are getting killed… but some where the bottom will hit and until then I will keep buying into it..

It does suck however to keep aggressively investing and still seeing a decline in overall value… I’d have been better putting it in the bank.. but who knows when it will turn around.

For the first time I have down several Tax loss harvest transactions this year which have worked out will for me since my exit and entry points were about the same value in the market and I was able to capture the losses on short term to negate against ordinary income!!!! So that was a win for me amongst the other chaos.

Also a great reminder for folks to reevaluate insurance. I did the same thing back in March this year and ended up with equivalent coverage at about $400 less in total premiums on my $1400 a year insurance bill so that was a nice adjustment.. Can you guess where that extra $400 went? Yup index funds!!

I was looking for your average Annual expenses you are currently spending and couldn’t find a number… Just curious against my own planning.. Do you have a post that details that analysis?

cheers!!

So Tim,

You’re happy to see we’re getting clobbered? Thanks buddy! 😉

If you don’t mind, when you talk about exit/entry points: Did you just sit out of the market and wait the 31 days or were you invested in something else in that time frame? I hate the market timing idea of being out of the market personally bit curious what others do.

As for details of our spending and investment account values, we’ve chosen to be vague about that for various reasons but may reveal in the future. I’m pretty bad at keeping secrets anyway!

Cheers!

EE

Well no one is really happy about it are they?? Atleast we are all feeling the same pain. However, I know long term the last few years growth is not sustainable and I do want lower cost basis on some of my purchases to this cycle is necessary.

There are a few things that I sold and Immediately bought something else within a day or 2. They were on my shopping list and their prices had come down below my price entry points. ( I do a big of individual equity purchases along with index funds.) I did purchase some ETFs with proceeds of my loss sales and shifted some things around. Probably over all my allocation might be a little out of the desired, but I do quite a bit of individual equity so my allocation is a hard thing for me to really nail down.

Since I still have income coming in I’m more focused on building and I can deal with market drops that way.. When I stop working I will have to really look at my portfolio allocation better.

Yeah, misery does love company. I do actually think there is some value to see that others are staying the course as the markets are sputtering along (or worse).

Agree that expenses will be a bit different in retirement. While some expenses will likely go up (primarily travel) many will go down (daycare, commute costs) and may go down substantially if downsize to one vehicle and smaller home which is one reason we only set a goal of 20-25X expenses.

Oh and no worries on the secret! I completely understand and was just curious. That is something else I’ve been trying to formulate. There are so many unplanned costs that come up in my budget it is really challenging to try and put a fixed number on it. I’m not sure I’ll ever be able to do that.

Especially when I start taking more trips and racing again.. I just want to have enough extra padding in there to cover those influxes and if need be make a little extra on the side to bridge the gaps.

Yay! you guys are back! This is one of my favorite blogs because it inspires me to save money in order to get started investing. Thank you for starting this blog, its good to know Im not the only one out there wanting financial independence.

Anthony,

Thank you for the kind words! Comments like this keep us going with the blog. Good luck on your road to FI and please continue to add your voice to the conversation.

EE

Welcome back! I usually wait until the last of trading for the year to make any tax related moves. You might find your 10k loss has turned into a gain by then!

That’s a good idea. Then I can just check it once at the end of the year and if any substantial losses just do it and be done and if not then nothing to think about. I think I’ll recommend to the Mrs. that we actually make that a part of our written investment policy. Thanks for the idea!

EE