February Update

Ugh!

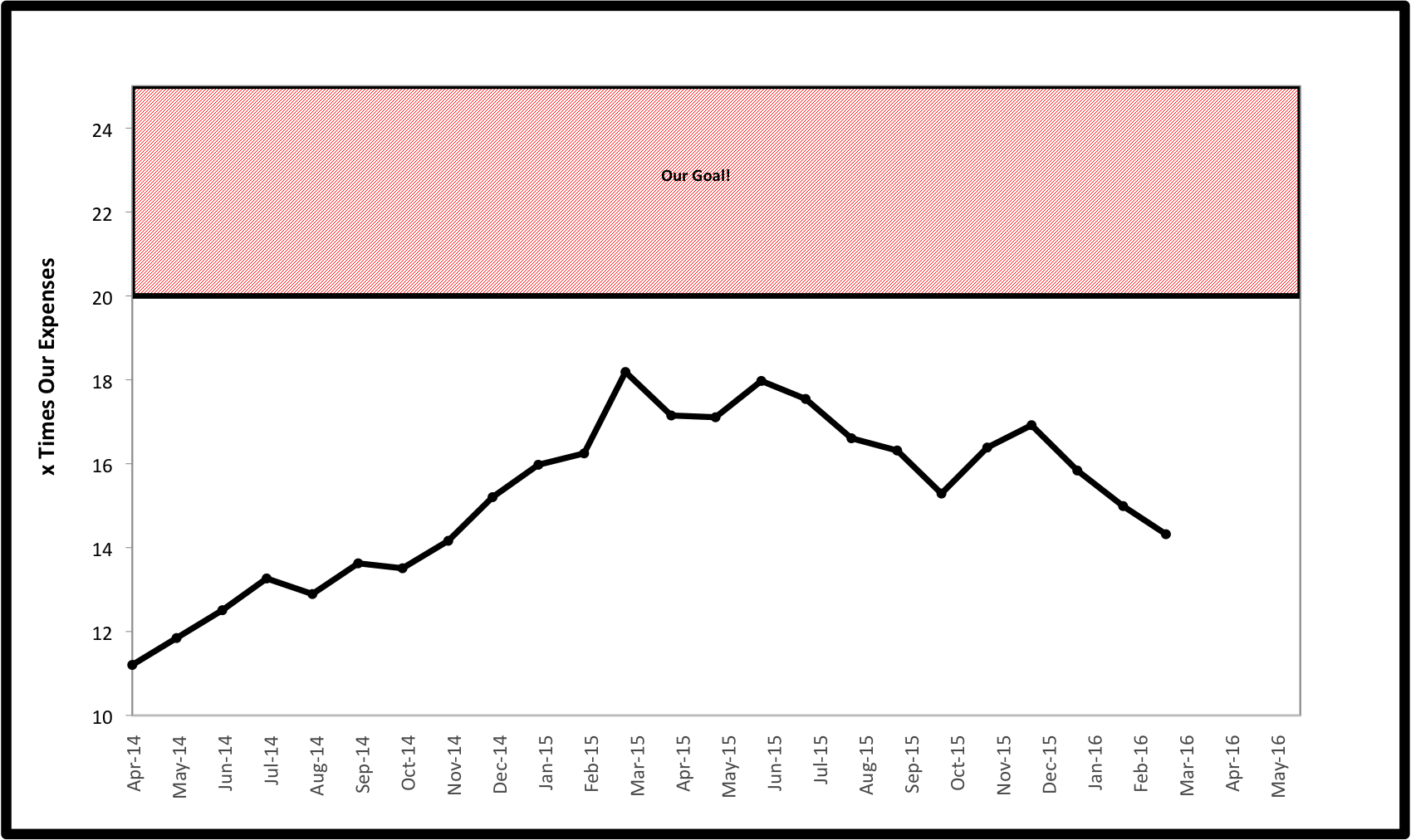

Our investment value actually went up a small amount this month. However, spending was up substantially compared to last February. This more than cancelled out our small gains. Our assets now sit at only 14.3X our annual expenses.

Our increased spending has been driven up by a combination of health related expenses. Our grocery bill continues to be over double what it was a year ago as we continue to experiment with changing our diet to address Mrs. EE’s auto-immune type symptoms. My contribution to insurance premiums has also more than doubled since the start of the year. We also have higher deductibles with this new plan increasing our share of medical bills which came due for testing for Mrs. EE. All of this goes to show how important good health is to successful early retirement and how vulnerable a plan can be to health care expenses, even if planned for carefully.

On a more positive note, we also had some increased spending due to taking our first ski trip west since having our daughter which was a really fun splurge and well worth every penny. We also made an unexpected fairly large charitable donation to an organization that we are involved with that is having tough financial times. Both of these instances make us realize that spending more can be a positive thing and this is again one of our values reflected in our future plans.

Is Your Plan Changing?

The recent drops in the markets have our numbers looking pretty bad. To recap, these numbers represent our investment assets as a multiple of our annual spending. We determine annual expenses by keeping a rolling 12 month average, updated at the end of each month. Our investments include stocks, bonds and cash which are used to produce income. Our residence, cars, other investments earmarked for Little EE’s future education expenses, etc are excluded from these numbers.

Less than one year ago we peaked with our investments at just over 18X our expenses. Since then, we’ve kept our overall spending pretty consistent. At the same time we’ve continued to contribute substantially to our investments by maxing out both of our work sponsored retirement accounts, maxing out 2 Roth IRA’s, saving the remainder of my paycheck and all of the money from our side-hustles in taxable accounts and reinvesting all of our dividends and interest. Tally it up and it is a sizable contribution. Despite this, our number has dropped and has been hovering in the range of 14-16X our expenses.

I know other people write about moving their retirement dates up when their numbers look good or thinking they may have to work longer when their numbers look bad. So are we changing our plans? Not at all.

I’m curious to hear how others are changing (or not) their plans. I am finishing up a post that explains exactly how we plan to live and fund our early years of our early retirement. Until then, here are a few random thoughts on this topic that will set it up and hopefully start others thinking and discussing this issue.

What Are Your Biggest Risks?

Almost everyone who writes an early retirement blog has written their take on using the 4% rule to guide how much money they will be able to spend in retirement. Using the inverse of 4%, the thought is that we will be financially independent when we have 25X our expenses in investments. Here is our stab at the topic from one of our earliest posts. We also wrote a post titled “Is a 4% Withdrawal Rate Too Much or Too Little for Early Retirement”.

We, like most in this community, spend a lot of time planning and thinking about the issue of how much money we will need to retire. (Like every month when we do these updates.) It is important. However, running out of money in retirement is only one risk that we face. Given our flexibility, conservative nature and understanding of our finances, I would say that the odds of us actually running out of money in retirement are minimal to none. This is in line with the thinking of Michael Kitces who argues that the whole idea of “probability of failure” should be replaced with “probability of adjustment” in this excellent and entertaining blog post about phrases that should be banished from retirement planning.

We outlined how we came to our FI date in this post. I more recently wrote a post called “Fail Upward” in which I outlined the many reasons we remain on this path. We are committed to our plan and FI date, whether we have 25X or even 20X our expenses saved up in investments by that time.

Waiting Too Long

Another risk that we face is waiting too long to leave our 9-5 lifestyle to pursue a different course for our lives. We have always been good at delaying gratification. We were the ones working multiple jobs in college while our friends were maxing out credit cards to go on spring break. We were the ones that were driving cheap, used cars while our peers were financing their luxury vehicles.

We don’t regret those decisions at all as they have been instrumental in setting us up where we are today. However, our willingness to delay gratification can make us too conservative. A couple of things have this front and center on my mind.

Our daughter is now three years old. This is a magical time and I treasure every second I can spend with her. It is amazing looking back at baby pictures that in my head seem like just yesterday and not even recognizing her as she has grown and changed so much. It kills me to know that she spends more time being raised by daycare and her grandparents than either of us. We know we have only one shot at any stage in her life and then that little girl is gone. We want to have the time to be there as much as possible.

I also have been watching my mom struggle with some significant health issues. My parents did everything “the way it should be done”. They are amazing parents to my brother and I. They have always been there for everything for us. They are extremely financially responsible and taught me the most important lessons that I now share on this blog about money and life.

After dedicating their adult years to raising us to the best of their abilities and running a small business, they were able to FIRE in a more traditional sense, retiring in their early sixties. This should be their time to kick back and enjoy life, travel with their friends, play and be active with their grandchild, etc. Instead while my mom is strong of mind and has plenty of money to do whatever she wants, her body is failing and it is painful for me to see.

As Mrs. EE began to have some recent medical symptoms of her own, it made us realize that our time and health is not guaranteed. The things that we love to do including hiking, climbing, and skiing are not guaranteed to be possible at some later time. While we know we must plan to live to 100 or beyond, not even tomorrow is guaranteed. We need a retirement plan that reflects that reality.

Not Creating Problems

We have been very fortunate. We have never had financial stress in our adult lives. We have had the amazing opportunity to do things that others only dream of. We have traveled the world, climbed big mountains, dove in the clearest oceans and saw amazing reef, hiked and backpacked in beautiful places, spent time in amazing cities around the world and attended major events such as Super Bowls and major concert festivals.

While we have evolved somewhat over time and learned to enjoy more simple pleasures, we are not frugal people by nature. We have never lived on a strict budget. We only in the past couple of years began tracking our spending. We don’t desire a life that is constrained by living on a fixed amount of money and is conducive to developing a “poverty mentality.” We don’t want to replace the stress of not having enough time to live the life we want to live with a newfound stress of not having enough money to live the life we want to live.

Our Plan

So to recap, as we developed a plan for our lives we are trying to balance these three competing issues. We want to ensure that we have saved enough. We want to leave the 9-5 rat race ASAP to create more time for our family and other interests we are passionate about. We don’t want to trade the stress of working for the stress of living on a fixed budget. In short, we want to make sure we enter our early retirement with a well thought out plan and not a mid-life crisis.

That is what we are thinking about as we begin to develop our transition into early retirement over the next year and a half. We will soon reveal more details of how we plan to achieve this. Until then, we’d love to hear what is important to you and how your FIRE plans are holding up or changing with the recent market volatility. Please share below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

No real changes here. Up or down, we’re still looking at outside latest of Aug. 2018. That’s assuming NO layoff for Mrs. SSC and her quitting next March with or without a package. We’ve also added rent for 3 years so we can de-risk moving to the mountains for a bit.

The only real change is like you guys we’ve realized we want more time with the kids and more time while we’re “healthier” than just assuming we’ll stay healthy into our golden years. This time next year, if the right job opportunity arrived, we would be fine making the transition, and moving out West a little early. That’s our only change. Otherwise, we’re going to just stay the course and keep waiting. 🙂

As I follow along with your blog and read your thoughts in the comments I think we’re really on the same page. Maybe we’ll end up in the same ski town in the next year or two. Any progress on finding a landing spot that looks appealing out west?

And I can’t help but butt in on this conversation. 🙂 We’ve scouted a whole bunch of the ski towns in the west, so let us know if we can help!

I will hit you up with a PM in the near future but our wish list is:

1.) Up close access to the mountains (less than 10-15 minutes)

2.) Affordability of housing/living.

3.) Schools

4.) Local Community, ability to walk or use public transport.

As of now, we are looking at

1.) Driggs, ID (Grand Targhee)

2.) Ogden, UT (Snowbasin and Powder Mt)

3.) Fraser, CO (Winter Park)

We are just in the early stages and open to any suggestions!

Being Healthy is indeed the most precious items to have in order to enjoy FIRe. I hope all turns out ok for MRs EE.

The recent market volatility has not interfered our FIRE plan. It i still too far away to have a real impact. A good correction is actually a good opportunity for us to buy more for the same amount of money.

Lately, we are thinking more in terms of living now, maximizing the now with a plan to FIRE in 2029. Just like you, we did our first ski trip with the kids this year and it was great. We would love to do these each year. That means a big chunk of money we can spend less on FI savings.

At some times, I doubt the FIRE plan: why not live now 150pct?

I do and don’t doubt the FIRE plan. The more I learn, the all or nothing of a traditional retirement seems to not make a lot of sense, especially for those of us with kids. However, getting to a point where you can work just small amounts and essentially have enough to not save any more or even spend down small amounts of investments seems to allow for the fastest and most secure path to a more balanced life. I don’t think it has to be live 150% now OR delay all gratification until retirement. We’re looking for that happy middle ground.

I’m also dismayed this month about the market reducing my investment stash. I continue forward progress, though, because of two decisions I made some years ago.

I saw large spikes in expenses like yours when our second child was born. My wife hates the idea of “early retirement”: she’s killed both earlier attempts so far with lifestyle inflation, and is zeroing in on my current try. I shifted our FI target to that lower, stabler set of expenses we’ll have once the nest empties.

I no longer track net-worth or investment value. Rather, I track the income I’m actually generating to use in FI. The typical accumulation seems to concentrate on building up value, with (at least partially) a conversion into producing income. I started that conversion very early. That effectively splits my “FI portfolio” into three parts generating income: one for living expenses, one making my discretionary budget, one making her discretionary budget.

Together, the track of my FI progress bounces far less than it did before. I feel much more comfortable with my projections because of that. Perhaps teasing out a stable core of expenses will help you project more confidently? I know having the split really helped me unmask several expenses which shifted from “living” to “discretionary” or vice versa, so I could adjust my targets to reflect that.

Interesting comment. Just curious why your wife is anti early retirement. It seems it would make it very difficult if not working toward the same goals. My wife was not so into this as me when starting out, but we managed to get on the same page and are working together to our goals. I would think that having financial goals that don’t match a spouses would be very stressful.

As for focusing on income, how are you doing that? Real estate? Dividend focused investing? I don’t like the big fluctuations that we experience with our method of investing and tracking but don’t have the time or energy for real estate at this point in my life ( though I am learning about it and may tackle it to diversify in ER). As for dividend investing, I think there are psychological advantages, but it would take considerably longer to accumulate a portfolio that would support us just off of dividends and focusing on income producing investments in taxable accounts while appealing in retirement seems very tax inefficient in the working years.

Thanks for the comment and I’m curious for any more insights.

Talking about moving our date around based on the numbers? Yep, busted. 🙂 We feel the clock ticking in a big way on the physical pursuits, too. I can’t imagine being 55 and still aspiring to lead 5.10. But who knows? We just don’t want to take that time for granted, and that’s a huge part of our motivation to hurry up and quit already. So much of what we want to do requires two fully sound bodies, and we don’t know how much longer we’ll be in possession of those! 🙂

When we got serious on our path to FIRE in September 2012, 2 things set that in motion. One was a positive, the birth of our daughter. However, the other was experiencing the death of my cousin and close friend in her early 40’s. She was a picture of health her entire life, was diagnosed with cancer and within 2 1/2 years died. Since then, I’ve seen my mom’s health problems, Mrs. EE’s recent problems and read stories like your own and it makes me realize that you can’t put life on hold forever, b/c forever is not guaranteed!

Really like the ideas in your post, especially the ‘probability of adjustment’. I think because we are all such ‘planners’ by nature, we have to remember that it is just that - a plan and be confident our future selves will be smart enough to adjust. We’ve got ourselves this far …

I love the “probability of adjustment” also. I have always felt that way but couldn’t quite find the way to verbalize it. I assume that there are people that cash out, have no idea what their doing financially and literally “fail” by running out of money. However, I doubt there are many people who know their finances like this community and build their wealth slowly that would allow that to happen without realizing it was happening and then make some adjustments to stop it.

Hang in there! The market is coming back in March. My own experience is that in times like these it’s best to lean back and not lose your nerves. Put more money to work when the market dips. Have you considered using the drop in the market for tax loss harvesting? That could reduce your tax liability, and those savings can be used to put to work before the market bounces back.

Best of luck and I really enjoy your blog!

Ern

Agree with your sentiments and your suggestions. We moved extra cash over and maxed out our Roth IRAs at the beginning of the year already. We also sold off a bunch of funds at the end of 2015 to lock in some losses and then bought them back at the end of January so we harvested already for tax purposes.