February Update//Movin’ On Up and Random Shout Outs

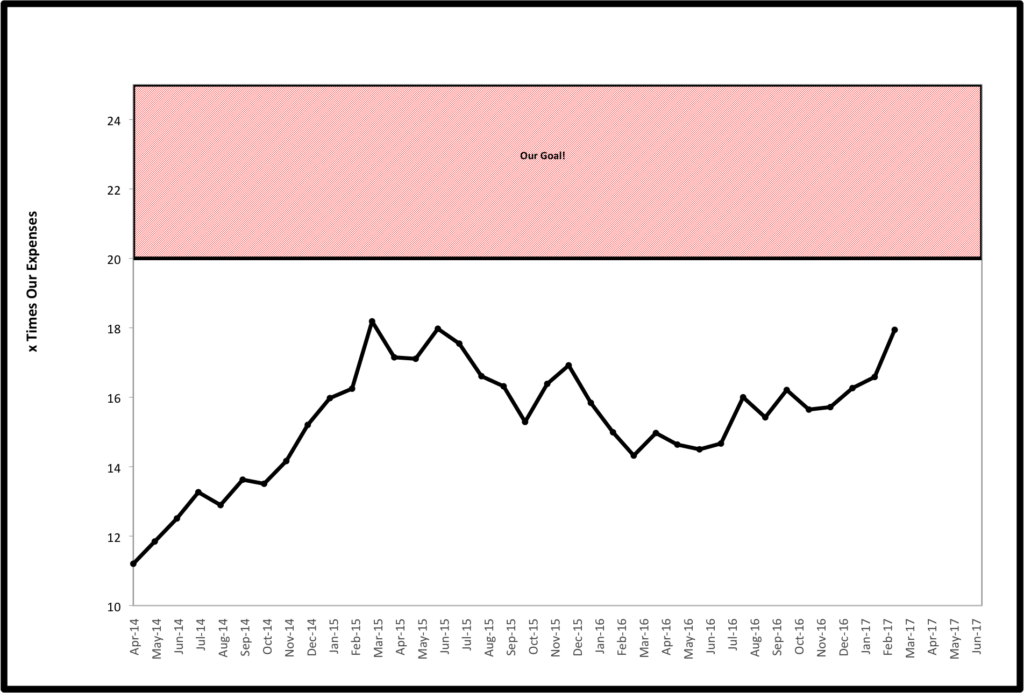

Well that graph is finally looking better. Our numbers were buoyed by a combination of a big spending reduction as compared to last February and a continued run on stocks sending our asset values on a continued upward trajectory. Last month our assets increased by 3.45%. Simultaneously, our annual expenses dropped by 4.3%. Add it up and our assets/annual spending ratio increased from 16.6X to 17.9X in one month! WOO HOO!

Well that graph is finally looking better. Our numbers were buoyed by a combination of a big spending reduction as compared to last February and a continued run on stocks sending our asset values on a continued upward trajectory. Last month our assets increased by 3.45%. Simultaneously, our annual expenses dropped by 4.3%. Add it up and our assets/annual spending ratio increased from 16.6X to 17.9X in one month! WOO HOO!

Over the past year, when doing these updates I felt like I was starting to sound like a broken record in explaining away our spending while watching our assets/expenses number flounder around with little change despite doing really well with our saving and investment performance. This month, we are able to demonstrate the opposite effect as our numbers took a big jump due to such a drastic reduction in spending. How did our spending decrease so much? That leads me to the first of a couple of shout outs for the month.

Shout Out to Travel Miles 101!

About a year and a half ago, I decided to try an experiment with travel hacking after reading so many bloggers write about how easy and lucrative it was. After my initial experience for our long ski weekend to Utah last February, I saw how easy it could be. I quickly earned and booked a free non-stop cross country flight for signing up for a credit card.

I also realized it is not simple. I screwed up my hotel booking and was unable to use my accumulated Hilton Honors points for two free nights hotel stay (a $300+ dollar mistake) and was unable to accumulate enough points for the other two nights we stayed (another $300+ expense). I was also unable to figure out what to do about a car rental (another $400+ expense for a 4WD vehicle in peak ski season).

When we returned home, I signed up for Travel Miles 101 Free Travel Rewards Course (no affiliate). We did essentially the same trip to Utah this February. This year, I was able to use the knowledge from the course to get two free cross country flights and 4 nights in a Hyatt hotel all on the points accumulated on one credit card, with about 1,000 points to spare. We then used a second card to accumulate enough rewards to pay for 4 days SUV rental with an additional $180 in travel credits left over for future use.

Figuring in retail price and taxes, the flight and hotels we booked saved us nearly $1,400. We were able to get these rewards by placing a little over $3,000 of our normal spending on one card to reach the minimum required to achieve the sign-up bonus. We paid no credit card fees or interest. This essentially gave us a 40+% refund on our spending. Getting a free rental car plus the remaining credits was a $520 value obtained on approximately $3,000 normal spending on the second card. Again we paid $0 in fees or interest. This is essentially a 17% refund on our spending on that card. Compare that to the 1-2% cash back credit cards we have been using for years.

Again, I have no affiliation with Travel Miles 101, but I do want to share this free resource. Big shout outs to Brad and Alexi who developed the course and website. I would strongly recommend checking it out for anyone who is interested but skeptical or who has struggled with figuring out using credit card rewards for travel hacking. The information we learned in the course is incredible.

On a bit different note, this situation also demonstrates with numbers just how expensive a standard American lifestyle is. Most of us work about 50 weeks a year, while trying to ram as much living as possible into weekends and a couple of weeks of vacation each year. In F.I.R.E., being able to flip that model on its head and live where we want to live and travel slowly and intentionally, we can permanently eliminate the need to have $2,000-3,000 weekends. Instead of paying $100/day/person for a ski pass, we can spend less than $1,000 for a season and ski unlimited days. Instead of paying money for a flight which is very expensive when prorated over only a few days, and then spending for hotels, rental cars, and restaurants for each meal, we can instead travel back home and spend long periods of time with our family very cheaply.

The combination of a major lifestyle change we have planned and the travel hacking skills we are developing can allow us to minimize, or essentially eliminate, this line from our budget for eternity while doing more of the things that we love to do. While it is possible to achieve FI by saving $25,000 for every $1,000 that you want to spend to live a typical American lifestyle, it can take years or even decades to do so. It is often times far easier to determine the lifestyle that you want to live, and then figure out alternative ways to have it other than paying retail.

Shout Out to Vanguard!

This past weekend I logged in to our accounts to do our annual re-balance and I saw a notice from Vanguard that several of the funds we invest in have had a change in fees. As I clicked on the box, I learned that the expense ratios on the Emerging Market Stock Index had decreased from .15% to .14%. Both the European and Pacific Stock Index funds decreased from .12% to .10%. While these decreases look tiny, they represent a 6.7% decrease on Emerging Markets and 16.7% on the other two funds. In the 4+ years that I have been investing with Vanguard, the expenses on all but one fund that I personally invest in have decreased substantially, while none have increased.

In a world where we are constantly bombarded with hidden fees and increasing charges, it is refreshing to work with a company structured to truly have the best interests of their customers in mind. While I know there are other reasonable options for investing your money outside of Vanguard , I don’t really see any reason to bother even considering them (again I have no affiliation or financial incentive to say this, but I wish I did!).

Shout Out to Physician On F.I.R.E.!

As regular readers of the blog know, despite being a blog about eating the FINANCIAL elephant, I’ve not been writing much about finance of late. I had found myself in a bit of a rut where nothing I was reading was really new or interesting to me. A rare exception of a money article that really made me think differently was POF’s recent post “My Money is Worth More Than Your Money”.

Many people, ourselves included, calculate their net worth without differentiating tax-free (going forward) Roth money, tax-deferred money, and taxable money. Some people, but not us, even count their home value in with their assets. Simply calculating your asset values or net worth by adding up the numbers you see on statements is a quick and easy way to see what you have. However, what you have on paper and what you can actually spend are potentially two very different things as POF points out in his post.

These assets will be taxed differently based on the laws that govern them and your personal income structure. A dollar in a Roth account is worth a dollar. A dollar in a traditional IRA could be worth a dollar, or $.85, or $.75, or considerably less depending on your personal federal and state tax situation. However, we have always struggled with finding a way to account for these differences, since we do not know what our future tax situation will be. Tax laws and rates are subject to change as are our annual spending needs.

While POF was not able to answer all of our questions in his post, he did give us a different way of looking at things and spurred me to think about and look at our investments in a different way. Mrs. EE added an equation to our investment spreadsheet, to show our percentage of money in each of the three categories. For those keeping score at home, after maxing out our Roth contributions when re-balancing our accounts here is where we stand: Roth 10.7%, Taxable 43.3%, Tax-Deferred 46.0%. Indeed POF, your money is worth more than our money. Thanks for giving us something more to think about and look at with our planning going forward.

Shout Out to My Pops!

A few months ago, I wrote a post outlining how my dad was using his own retirement to serve others working as a Court Appointed Special Advocate (CASA). The post generated only a few comments, but those that did respond seemed to have strong, emotional responses based on their experience with the system. I therefore wanted to give a quick update on the situation.

This past month, the boy’s father went before a judge and was granted full custody without further supervision. After a long winding road, this story has hit a happy milestone. The moment was a bittersweet one for my dad. While this family’s story is far from over, it is over for my dad in his official capacity as a CASA. Shout out to my dad for a job well done, and hopefully for inspiring some of you who read his story to consider serving kids in desperate need in a similar way.

This is also a reminder for many of us that start down this path to FIRE seeking happiness or satisfaction. If you are struggling to make yourself happy or satisfied, perhaps you should try to focus your attention away from helping yourself. Instead try helping someone else. You may be surprised what happens next.

(P.S. Pops, If you and mom are looking for a new non-paying job working with demanding and at times emotionally draining people, we’re looking to fill an unpaid nanny position based out of northern Utah.) 😉

Has anyone else taken the Travel Miles 101 course with similar results? Am I wrong in my blind love of Vanguard? Has anyone figured out a good way to value assets based on tax status, or do you simply calculate net worth? Anyone thinking of new ways to use your money and/or time to give back to others in unique or interesting ways? Share your thoughts below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

Mr. Picky Pincher’s 401(k) is with Vanguard and we love them. 🙂 We plan on investing more with them once we pay off debt!

Wise move in my book Mrs. PP!

Applause to your Dad. A remarkable person being a CASA. Have only minimal experience helping others by volunteering. it’s the most rewarding & gratifying time.

Agree Evie. Volunteering more is one of many things I plan to ramp up when I actually have some time to breathe in a few months.

Cheers to a rewarding February, successful travel hacking, a caring father, and Vanguard’s low fees!

Regarding your money versus my money, we’re both in excellent shape from a tax diversity standpoint. Having > 50% in Roth and taxable sets you up nicely for easy access to funds in early retirement, and low tax rates. I’m sure you’ll have the option of low-cost Roth conversions of the tax deferred money, as well.

Best,

-PoF

Agree. The tax planning mistakes (or more accurately complete lack of a tax plan) in the first decade of our careers is the difference between not quite being FI yet and having achieved it years ago. That said, our position of having a large percentage of our money in Roth/taxable accounts will give us a lot of flexibility and tax planning diversification post FI.

Thanks for the travel hacking resource. I’ll definitely check it out. I’m by no means an extreme travel hacker but have taken advantage of plenty credit card points over the past few years. Always fun to book a free trip!

The cool thing about the course is that it teaches some very advanced and some very simple techniques. We keep it extremely simple and even at that it is pretty easy to rack up a couple grand in rewards in a year. Definitely worth the couple of hours of time to go through the course.

“It is often times far easier to determine the lifestyle that you want to live, and then figure out alternative ways to have it other than paying retail.” I really liked this and its very true. Paying the “retail” price for everything is why most people are broke. With smart spending and self control you can really have the lifestyle you want for much less. Question everything, comparison shop, negotiate, learn to DIY. With a little extra effort, you’d be surprised how much you can save.

Agree Arrgo that this is the essence of FIRE. Simply figure out what you really want and then learn to look at the world in ways different from the masses and you will find opportunities everywhere to make amazing improvements in your lifestyle without needing massive spending to do it.

I like that inflection point on your graph… keep on keeping on!!

Also yes.. season passes and a side gig at the mountain are the way to go… I have got in 47 days of skiing and riding this season so far.. and I am net + $2700.. after expenses..

Pretty cool to hear that Tim as things are quickly moving from the way I think they theoretically should go, to actually putting the plan into action!

Assuming no major crash it should be even much better next month as our old investment expenses and the tax consequences associated finally come off of the books from last March, meaning another drastic drop in spending.