March Update//Trusting Your Process

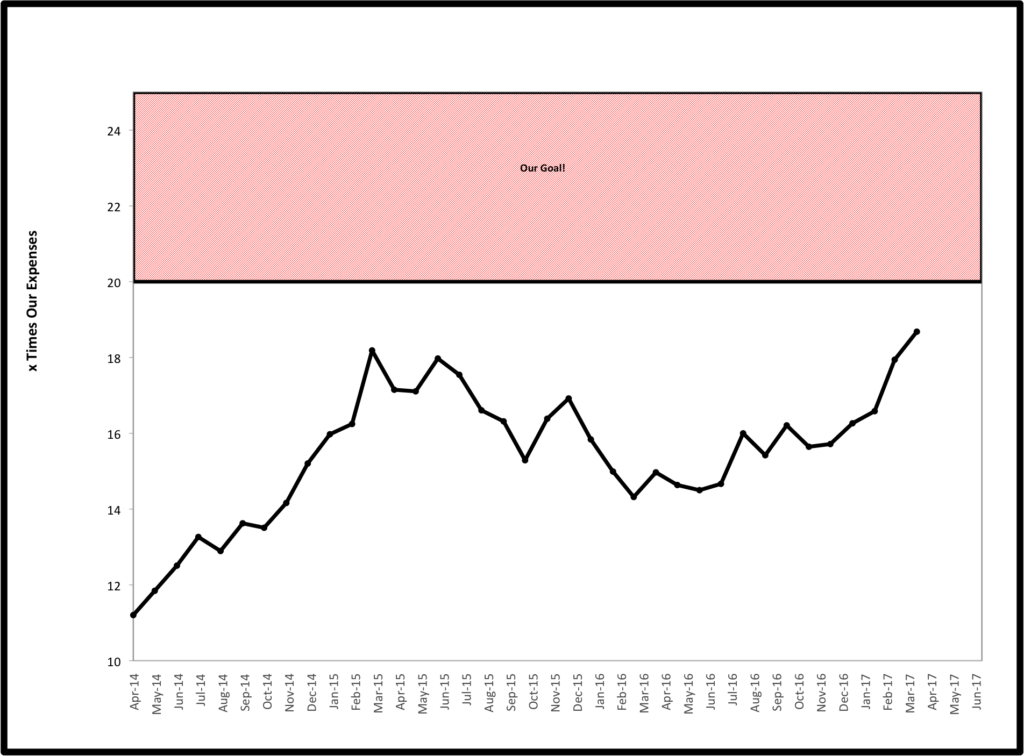

Our assets as a multiple of our annual spending have reached their all-time high at 18.7X, up from 17.9X last month. This 18.7 number is actually artificially low as we’ll show below.

Breaking Down The Numbers

On the assets side, there was not much change. Our portfolio was up by .82% over the past month, bolstered by continued regular contributions, quarterly dividend distributions and a strong performance by our international funds. This helped to overcome a sub-par month for domestic stocks, bonds and REITs.

On the spending side, we spent nearly twice in March what we had in January or February. One expense that occurs every March that increases our spending is paying our property taxes.

However, $1,300 of our high spending this past March was a charitable contribution and another $700+ went toward our annual ski passes. Last year, both of these expenses occurred in April, so they are “on the books” twice in the way that we keep a rolling average of our annual expenses. Take that $2,000 off of our annual spending and our 18.7X number would look even better.

We also spent $450 for a cross country flight for a summer trip to scout out our likely future home, which we will be sharing in detail after the trip. As we shared in our February update, we have been developing our travel hacking skills. This $450 should be our only travel expense for our twelve day trip as we were able to cover the other two flights, 10 nights in an Air BNB, 1 night in a hotel, and a rental car all completely free with credit card rewards points.

Our other unusual expense for the month was a $431 income tax bill. We wrote over a year ago about finalizing our divorce from our financial advisor. For the first time ever, in 2016 we were free of the effects of holding and/or selling off the costly and extremely tax inefficient actively managed funds held in a taxable account as recommended by our former advisor. As a comparison, our tax bill last March was $4,132.

By ridding ourselves of these funds and implementing our simple tax efficient investing strategy, our tax bill dropped by a whopping $3,701 in year one of our financial advisor independence. While it will be exciting to reach true financial independence, finally being financial advisor independent is a great feeling and a big step in the process! Sayonara, Adios, and Bon Voyage financial industry (and massive fees and tax bills that come with it)!

All in all, despite our “accounting errors” on the charity and ski passes and increased travel expenses, overall March expenses were over $2,000 less than last March due to the tax savings, spurring the uptick on the graph in a pretty flat month for asset values.

Trusting Your Process

We feel it is important to share our numbers in these updates, warts and all, to help others to understand that the path to financial independence is not the smooth upward climb that we all would like. Take a quick glance at that graph and you will see many ups and downs.

We are basing our numbers and goals for financial independence around the idea of 4% safe withdrawal rate research. However, it is importance to grasp that investing in volatile assets is actually less risky over time than “safer” (i.e. less volatile investments). It is also important to grasp that life happens, and so spending needs change and at times can be volatile as well. We have tried to develop our “ultra-safe early retirement plan” to reflect both of these realities, while allowing us to make major lifestyle changes prior to achieving assets 25X or greater as would be suggested to be prudent by the 4% rule.

As we have been sharing over the past year, we have had our frustrations as we wanted to see our numbers increasing steadily and that was certainly not always the case. This is where it is extremely important to understand the story behind the numbers. Without context, it would be easy to become frustrated and lose focus.

Seeing The Big Picture

It is vital to track your spending to see where your money is going on a monthly and annual basis. Otherwise, it is difficult to improve and virtually impossible to quantify any progress.

However, it is also crucial to not make the mistake to become overly focused on your current numbers as we did early on in this process. This is a near certain path to frustration and unhappiness. Instead, figure out what you truly want and then figure out a way to optimize spending to get there. Realize that there is nearly always a way to afford what you truly want in life with a little bit of effort and creativity.

One example for us was Mrs. EE getting stressed out watching our grocery bills double as she started a mostly organic, minimal grain diet to try an alternative approach to combat autoimmune symptoms she was experiencing. Over the past year, we have figured out ways to optimize our shopping to eat far healthier than we had before with minimal increase in spending as outlined in this post.

Our efforts with optimizing travel expenses as outlined last month, and our ongoing process of taking control of our investing and tax planning are other examples.

Truly understanding why numbers are what they are and being able to see the big picture is vital to stay on course, or make rational decisions to adjust course when appropriate. This has been vital to avoid getting too low when our numbers were looking ugly last year. It also keeps us grounded and sticking to our plans when our number start to look up as they currently are.

Do you agree that managing emotions is as important and difficult as managing savings rates, investments and taxes on the path to FI? What are your secrets to staying objective and on an even keel in good times and bad? Share your thoughts below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

Great post. Can I ask what credit card’s points you are using for the AirBnB? Is it the pay with American Express Membership Rewards points option? Looking to book an AirBnB soon and not sure if that is the only way to use points to do that, or if there are other more creative options out there. Thanks!

We just used the rewards from the Barclay Arrival+card which are worth more if used for travel expenses. You just have to make sure the billing party codes the expense as travel or the points are not worth as much. Hope that helps.

I think you have the right perspective. Just focusing on your number all the time will lead to stress and frustration as you mentioned. If thats the case then maybe you should work a little longer to create a bigger buffer for yourself. I just set my account contributions on automatic for many years and it worked out really well. One thing I focus on is keeping expenses and spending in check. Review and question what you are spending on. Challenge your bills. With a little effort you will be surprised at how much you can save. Its all about having some self-control and the proper mindset. You dont have to be super frugal or give up much. Its just cutting out a lot of ridiculous spending and not letting these companies control (or get-over) on you. This way you can feel like you are doing things right and have more control over your finances and future.

Agree and disagree on automation.

On the agree side first. For the first decade of our lives, we had an incredibly simple system. Live off the wife’s salary. Use my salary to put one paycheck to rapidly pay off mortgage and give the other to our advisor to invest. No investing plan, no budget. It worked well to build a decent nest egg and we were very happy as we never thought about money.

On the disagree side, by not educating ourselves and not paying attention to where our money was going we paid way more taxes and investing fees than was necessary and set our FI back by years. We also were very inefficient on everything from phone plans, cable, utilities and insurance which added cost to our lives with no added value. By fixing these issues we gave ourselves extra years of financial freedom and greatly reduced ongoing risks.

I think the key is to find a happy medium. Learn to address the big things that really make a difference, then don’t sweat the little things trying to be perfect. Also look at budget and investment performance 1-2X/year to optimize, vs. watching as closely as we do for the blog sounds about right. When looking frequently, the ups and downs are more pronounced. When stepping back and looking at bigger intervals, the path to FI will look much more smooth.

great sub title: trust the process… I recently developed a strong believe in that.

The graph hits the right direction again, creeping higher and higher

Thanks AT. I agree that is a big key to success.