December Update

Thank You!

It is that time where we share our progress and a few ideas or actions we’ve taken over the past month.

Before that, I want to take a minute to say thank you to all of you who were kind enough to take the time to comment or send us private messages in response to the November update in which Mrs. EE shared a bit about the health and diet issues she is struggling with.

We were overwhelmed by the number and quality of responses we got ranging from the simple “Hang in there!” to several page long e-mails with some awesome resources and specific tips and advice.

We tried to respond to every comment and e-mail individually. In case we missed anyone, it was simply an error of omission as we printed out many of the longer e-mails, read them and took notes on paper and came back to reply. If we missed anyone (or even if we’ve already told you once), THANK YOU! All of your support and input is greatly appreciated.

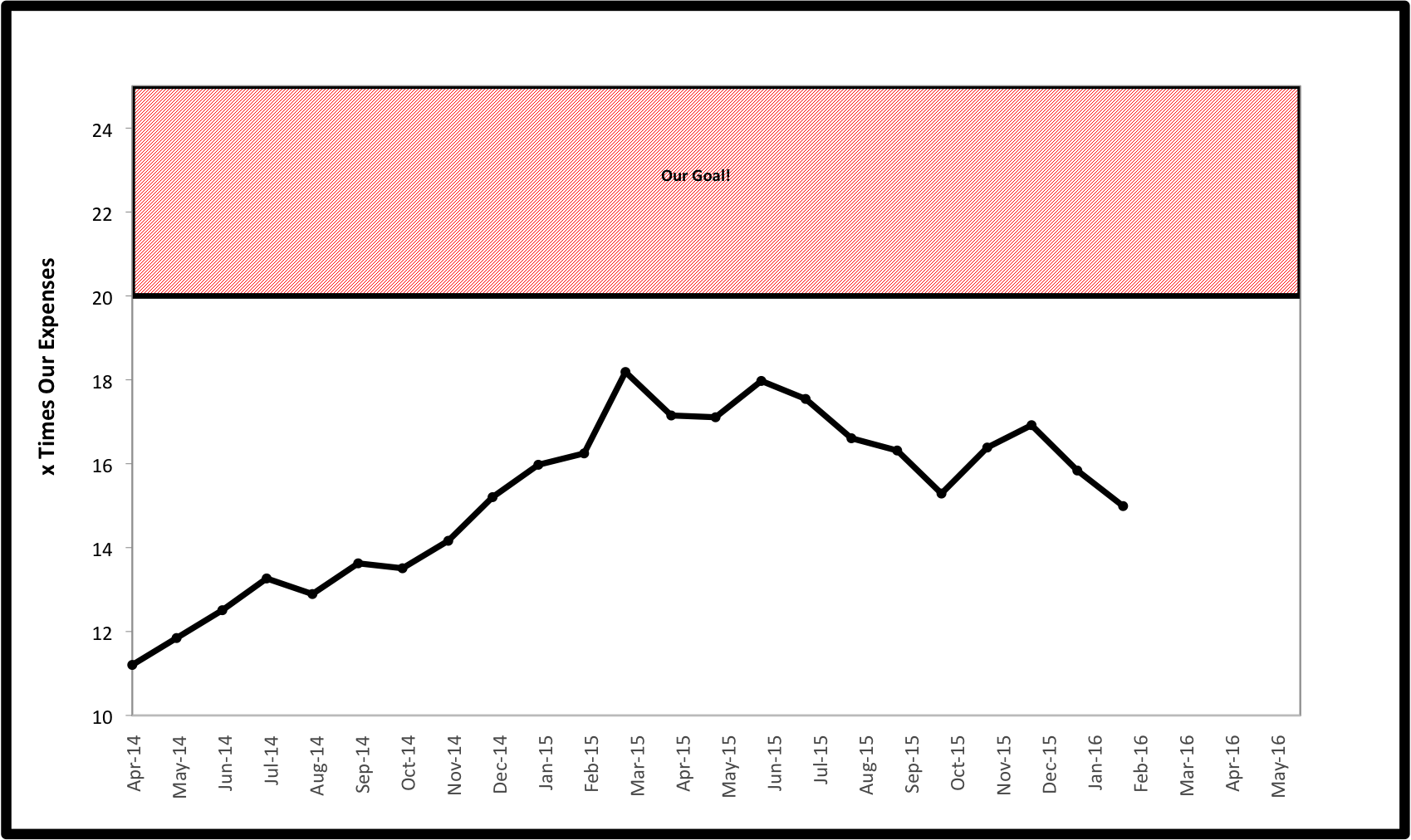

About That Graph

Ugh. Our assets as a multiple of our spending fell from 16.9X to 15.8X in one month.

We did poorly on both sides of the equation. It was a bad month across asset classes dropping asset value by .53% despite continued large contributions. Meanwhile our spending was up substantially. The spending was a result of continuing on a more costly diet, taking a much-needed family vacation, paying an outstanding bill that we finally received for some housework that had been completed back in September and some increased year-end charitable donations.

Knowing What I Don’t Know

One of the hardest things about managing your own investments is admitting what you don’t know and following a set, mechanical plan. Reflecting on this year’s investment returns is a good example of that.

At the beginning of the year, if I was a market timer and had to predict and sell one of our investments which I thought would have been the big loser for the year, I would have guessed REITs. Coming off a year of 30+% increases, and with a 5 year return up over 70% it had the look of an asset poised for a fall. Instead it was the class in my portfolio with the best return. (With a return of just better than 2%, maybe a better way to say that is it was the least bad.)

On the flip side, if I was a betting man, I would have guessed that international stocks would be carrying the year for us after everything domestic did well in 2014. Well it is good that I’m not a betting man as international was down big, with Emerging Markets down a whopping 15+%.

Overall, I am a proponent of not paying too close attention to what your investments are doing in the short-term and not tinkering. You could drive yourself nuts worrying about things out of your control. However, once in a while it is worth taking a look at to remind ourselves of how much we don’t know. As for us, we’ll be sticking to our boring plan, controlling the things we can and ignoring those we can’t.

Out of Here “Losers”

Speaking of things we can control…

A few months ago, we wrote about pondering tax loss harvesting and at the time we decided it wasn’t worth the effort for a minimal gain. In general, I think that tax loss harvesting is overvalued, especially as it is being sold as a benefit of robo-advisors by companies like Wealthfront and Betterment. Michael Kitces, whose blog I regularly read and I think is one of the smartest people in the financial advising space, offers some interesting insights and analysis here for anyone interested in a deep dive on the topic of tax-loss harvesting.

When I wrote my original thoughts on the topic, I received a comment from fellow blogger Financial Velociraptor who suggested looking at your cost basis once at the end of the year and then making a decision to harvest or not. While this goes against everything that you read about constantly monitoring for losses to maximize harvesting opportunities, it made total sense to me as someone who wants to be a passive, hands off investor. It prevented me from driving the Mrs. nutty with my overanalyzing and trying to pick the perfect time to harvest. It also is consistent with Kitces’ ideas that harvesting is generally overrated and so not worth spending a ton of time and stress thinking about.

At the end of the year I took a look and realized that I had a perfect storm and so pulled the trigger and sold off a bunch of losers in our international funds to harvest a large loss. I felt that this opportunity represented a perfect storm for us for several reasons and may be the only time we ever tax-loss harvest.

- Tax-loss harvesting is really a tax-deferral strategy. You are simply selling off your losing funds and buying a similar investment which is highly correlated but not identical to the original investment. Thus, you are lowering your cost basis for which you will have to pay taxes later. We are in position to maximize tax-deferral as this is one of our last years that we anticipate having a large income as we near our FI Day.

- The benefits were large as we were able to cancel out about $12,000 in gains from old actively managed mutual funds we sold off earlier in the year. We were sold these funds years ago as sold by our former financial advisor. (If you don’t understand why you don’t want to hold actively managed funds in a taxable account, you should read this.) Thus we saved ourselves about $2,000 in taxes for taking less than 30 minutes to analyze the situation and make the trade. If anyone knows of anywhere else I can get that rate of return, please contact me!

- There was no cost and little risk of tracking error as we did the trade all without cost within our Vanguard account.

Becoming a “1 Percenter”

As you can tell from the graph, I am unfortunately not writing about our wealth growing so much that we are now in the top 1% in the country. Fortunately for you, I am sharing one of the most simple tips that any reader of the blog can take to use their money to make a little more money.

We have traditionally kept an emergency fund of 2-3 months of cash on hand in a local bank. Now that we are approaching our early retirement, we have decided to up that to 5% of our total investments which means 1+ year of our normal spending will be kept in cash going forward as a buffer against market swings. This has us thinking about how to make a little money on this now substantial amount of money that is just sitting there at pathetically low interest rates of <.1%.

We looked into CD’s which still don’t yield even 1% unless we tied up our money for over 2 years. However, several online banks are offering 1% savings accounts with no fees and the ability to link to your other accounts for free.

1% interest rates will not make anyone rich. However, it is a free couple hundred dollars every year which over time adds up. Also, it is important to note that online banks, like brick and mortar banks, are FDIC insured so you are taking no extra risk for this 1% premium. To us this made it a no brainer as the effort to switch is minimal.

Happy New Year!

How was your 2015? Are you making any year end/beginning changes to your financial plans? Any big 2016 goals or resolutions you’d like to share? Comment below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

Hey you are doing the right things for sure… but 2015 was yet again a challenging year.. more so than in 2014, 2013, and 2012… those were easy years to make money.. I missed my targets for covering expenses and networth.. but as of October I started to think more on the expense side… and paying off the debts rather than trying to invest a lot and plan or hope for market gains… I’ll let that take a back seat and keep contributing but going to focus on getting my over all debts down to say $50k in the next couple of years. cheers!!!

Here’s my input Tim. I think we can drive ourselves a bit crazy trying to time the market and figure things out that are out of our control. I think that as long as you are making progress towards your goals you are doing the right thing, whether it ends up being optimal or not you can’t know until after the fact. If you said you were going to stop investing to sit in cash or worse off just spend the money b/c you were dissatisfied with the markets returns I’d think you were making a mistake. However, if you have somewhere else productive to apply your money, as you stated in paying off debts, then I see no reason not to do that. We just try to develop a plan and stick to it unless something has fundamentally changed. I think it is pretty easy to think we’re smarter than we are and it is good to realize that at times as I tried to show in the post.

Best,

EE

Happy new year, EE family! I’m sure that downward sloping line on your graph in December hurts a bit, but I know you’ll bring it back up no problem. Good to hear your take on tax loss harvesting. We’ve avoided it for two reasons: 1. Too much trouble to do the analysis, and 2. We actually want our cost basis to be high rather than low when we retire so that we can keep our capital gains minimal and our taxable income super low for Obamacare purposes. If we have a lower basis and higher gains, that could mess it all up. I think your approach to it — doing a one-time transaction — makes a lot of sense. The only other changes we’re making this year, other thank increasing our savings to consume our small raises, is to put money into Vanguard as we have it, instead of continuing to dollar cost average, and to start thinking more about holding more in cash, like you guys are doing.

Thanks for the input. I think that what you are doing is really smart. I love your big picture approach to your planning. I compare much of the writing about tax loss harvesting, and personal finance in general, to be taking small actions to feel good now without looking at how decisions made will effect you down the road. I appreciate the feedback and welcome any and all insights that can make us think on a deeper level.

Happy New Year to you as well.

I feel like an internet celebrity now. Thanks EE!

Ha ha. You have a low bar for fame but you’re big time in our little corner of the web anyway!

Thanks for the yearly update. I made a couple bad moves myself in 2015 trying to “time” the market without realizing it. Invested in international funds at the worst possible time. The goal was to balance my portfolio correctly, but it was just bad luck.

Yeah, we end up unintentionally timing the market by selling off our old managed funds when the timing is right for tax purposes or buying more shares as soon as we have some extra money. We never make those decisions based on trying to pick the right time, b/c obviously we don’t even pretend to have the ability to be able to do so!

Best!

EE

Hey EE family,

Best wishes for 2016! the graph of your net worth is a good summer of the 2015 volatility. In the long run, the 2015 small downward trend will only be a blip on the screen… I am sure.

As long as you keep doing all the right things, you will be fine. As you are mechanical about your investments, you should be ok. And spending some money on improving the house or a family vacation are things we do as well. They add to the value of life now! You future self will be happy with the memories of the 2015 holiday AND the big nest egg you pass on. Both are equally important.

AT

Thanks for the positive feedback AT. Best wishes to you as well for a great 2016!

Interesting post! What are your thoughts on using robo advisors to automatically manage your tax loss harvesting?

Sounds like you have a great mindset when it comes to making investing decisions i.e. ignore the things you can’t control. I think the market timing thing is tricky, because its really biologically hardwired into us to try to “time” the markets and convince ourselves we’re *taking* control, even if we know better.

I think winning poker players have a mindset that’s useful for making investing decisions. Poker and the markets are similar in that there is so much variance involved, that its very easy to think you’re “winning” - even when you’re making terrible decisions.

The way most people think about poker (and the stock market) is that they try to win each hand. They base their success on whether they won the hand - even if every decision they made was theoretically incorrect and would lose them money in the long run.

But professional poker players don’t look at it like that at all, they ask whether the decision they made was +EV (had positive expected value). From that point of view, you can make a good decision but still lose money in the short run, and you can make a bad decision, but still win money in the short run.

Easy in principle to understand, but of course 2 things make this really difficult in poker:

#1. In poker, its very hard to tell if you made the +EV move without rigorous analysis after the fact.

#2. Like with investing, most people get a “rush” and a feeling of success when they make money, and they feel a pit in their stomach when they lose money - even if they made the objectively “right” decision. This hardwired rewards system causes most people to “chase” winnings, against all logic.

When you look at it this way, I think investing in equities looks relatively simple by comparison.

For #1: although knowing if you made the right decision is very challenging in poker, we can make it super simple in investing by simply making fewer decisions.

We know in the long run, the markets always go up. We also know that because of transaction and opportunity costs, its a -EV (negative expected value) move to try to time the market for the retail investor.

Sadly, a lot of people don’t really understand this (especially since the media reinforces short term thinking) and think they “won” big picking stocks or timing the market, when in reality they’re just in a 6 year bull market. But I think pretty much anyone reading this already has #1 covered.

For #2: There’s no simple answer for how to prevent emotions from overriding logic, it really depends on the individual. But avoiding financial headlines, not checking your portfolio constantly, and having an asset allocation that’s in line with your own risk tolerance and investment goals is probably a good start =)

Sorry if that analogy is a bit of a stretch for your audience who already understand all this, but your post got me thinking =)

Nate,

I agree with your comment #1 100%.

As for your #2 I would add that it helps immensely to take the time to sit down and develop a written plan based on sound logic and not emotions and then actually having the discipline to stick to it when emotions can get involved. Here is ours:

http://eatthefinancialelephant.com/the-elephant-eater-investment-plan-and-asset-allocation-2/

As for roboadvisors, I feel that they are a great option compared to using a traditional financial advisor for those that are not willing to take the time to become DIYers. That said, I think that the effect of tax loss harvesting is overstated as it is only valid for taxable accounts and most people have most of their savings in 401(k) or other work related alternatives. Even if you do have large taxable accounts, as stated in the article tax loss harvesting is not a no-brainer as it is merely deferring taxes by lowering your basis which is not great for everyone. Also, if you have both work related retirement accounts and taxable roboadvisor managed accounts, you still have to be careful as you can get yourself in tax trouble if they are buying and selling in your taxable account for harvesting purposes while you are buying the same investments in the retirement accounts.