August Update// Mixing The Math and Emotion Of Retirement Planning

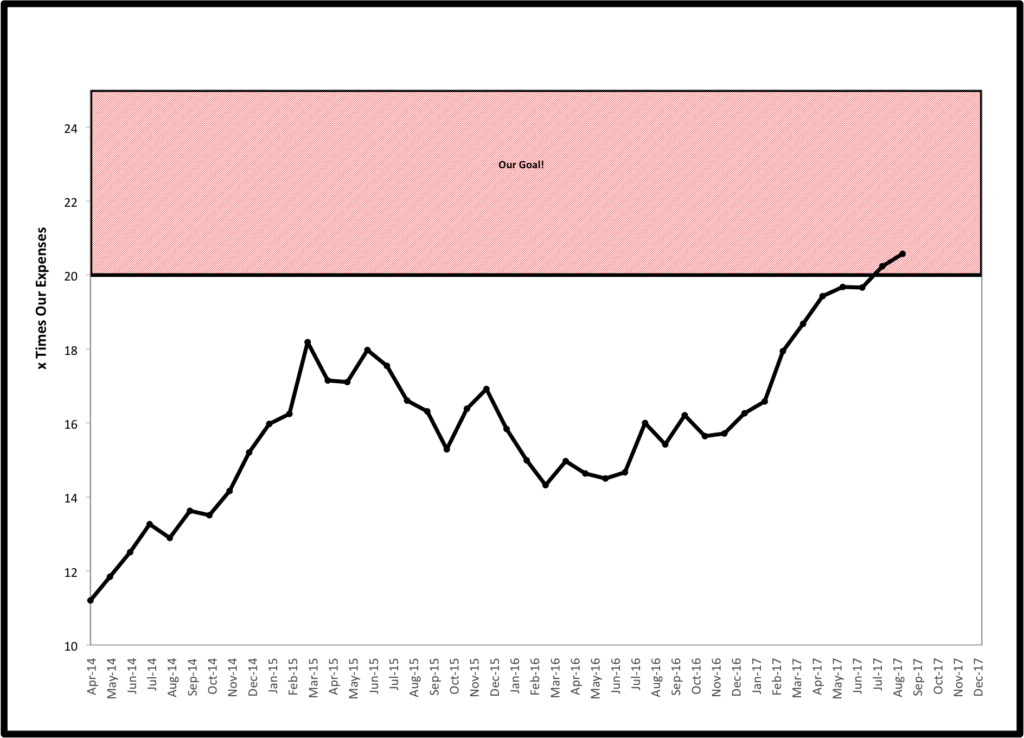

Continuing Upward

Our chart took another small tick upward this month. Investment values rose .91%. Expenses were very consistent as we spent $30 less than we did last August. Add it up and our assets as a multiple of annual spending improved from 20.2X to 20.6X.

As projected earlier in the year, our month to month spending has been steady or decreasing over the past year even as our lifestyle improves. Our spending on food continues to trend downward even as we eat a progressively more organic, lower carb, whole food diet that most people would associate with high costs. We also just did another long weekend with free hotels thanks to our continued success with travel hacking.

The only area that my short term spending predictions were wrong is that commuting costs would be eliminated, since I continue to go to work daily. 🙁 On that front, I did meet with my boss this past week and increased my 401(k) contributions. This will allow me to max out my plan for 2017 before finishing up working in the end of November. 🙂

Work and Retirement

Last month, I wrote a bit flippantly that in a worst case financial scenario that an early retiree could “just go back to work”. A reader, Donna, called me out in an excellent comment. I am grateful for the feedback, as it challenged me to be a better writer and better explain my position. She wrote:

“Ah, yes, but don’t forget to consider that if the “financial world starts collapsing around you”, it may be a lot harder to just “go back to work” making the same salary you make now. If I were out of the IT field for 5-10 years, my skills would be way out of date and employers in fields that change rapidly will probably not hire someone who’s 50-60 years old with that kind of gap in work history.

I think a lot of FIRE folks in their 30s or 40s always project ahead to their 50-60s, and picture themselves feeling exactly the same as they do in their 30s and think they can just pick up where they left of in their higher-paying careers if they need to. But trust me, for the average person, if you’re tired of the grind when you’re 40, it won’t be any better when you’re 55. ?”

I can not agree any more with this comment. However, we have already cooked this thinking into our “Ultra Safe Early Retirement Plan”. Yesterday, I had a post published at “Can I Retire Yet” that expanded on this idea. It explained how we redefined retirement to allow us to change our lifestyle both sooner and with more confidence than we could have with a more traditional retirement.

Because we plan to continue to pursue projects that are interesting to us and add value to others, I do actually think it will be pretty easy for us to find paid work if we need to. To flip that, I think the type of people that we have become on the journey to FI will make it hard for us to not make some ongoing money.

The 4% Rule and The Math Of FIRE

Recently, the Mad Fientist interviewed Michael Kitces, who has done substantial research on the math behind retirement planning. While the whole interview is excellent and highly recommended, the big take home point that is relevant to this discussion is that even small amounts of “post-retirement” income radically change the retirement planning equation.

To Donna’s point, we may not be able to go back to similar jobs making similar salaries to what we are now. However, this is the beauty of our plan.

By building our assets to be at or near FI, we can eliminate the need for ongoing saving. Savings and income taxes represent the vast majority of where our current income goes. Eliminating the need to save eliminates the need to make high incomes, and thus avoids paying taxes at high marginal tax rates.

We can make 25-30% of our current pre-tax household income and get by without touching investments. We can make 10-15% of our current income and live strictly off of dividends and interest from our investments without spending a penny of our principal. In our minds, this is about as safe as it gets.

Math + Emotion = A Good Plan

When starting out, I think that we got overly focused on the math of early retirement. We thought that FIRE was simply a matter of mastering investing, taxes, and safe withdrawal rates.

However, there is a large mental component to this whole process as well. Often there is a feeling of overwhelm for those trying to get started. This can be followed by over-romanticizing retirement as we get some wins under our belts, creating the mental challenge of being satisfied and happy while on the path to FI. Then fear and anxiety start kicking in as it comes time to pull the trigger on making major life changes.

Having a solid plan means having a solid grasp on the math of retirement and mastering your personal numbers. However, it also means thinking long and hard about the mental components to get started, stay on course, and then not get caught up in fear and anxiety that lead people to be afraid to make changes.

For more on the topic of mixing math and emotion of early retirement, click over to “Can I Retire Yet?” to read my newest post “Conquer 3 Criticial Early Retirement Challenges by Redefining Retirement.” Then let me know what you think below.

*Thanks for reading. If you enjoyed this content, you can find my current writing at Can I Retire Yet?. Enter your email below to join our mailing list and be alerted when new content is published.

Top recommendations

I read your article on Darrow’s site and thought it one of the best treatments of the real issues relating to the RE part of FIRE. My battle is primarily with what to do with my time. I’m working on it, but until I figure it out, I’ll continue to work (fortunately, I enjoy my job). We focus so much on the FI stuff sometimes that when we get there, we are not sure where to use that energy. A first world problem, for sure.

Thank you! I think I have the opposite problem, which is that I have too many things and I am having a hard time deciding what I want to pursue first. This is why I think a traditional retirement doesn’t really make sense for me and would not solve my problems.

Agree that either way that these are first world problems, but don’t think they are trivial. If you look at statistics on things like the number of Americans on anti-depressants, anxiety meds, etc. they show that a lot of people are struggling in life, despite living in a very prosperous “1st World” society. These problems are real and deserve ongoing exploration and discussion. Thanks again for the feedback.

Only needing to make roughly a quarter of what you do now to support yourself is incredible! Buying two years in this way, should there be a recession, will likely make your SWR so daggone secure it’s ridiculous.

Agree ZJ. That is the math side that makes a lot of sense and allows for decreased stress and increased prosperity, where in my mind the math of traditional retirement is extremely challenging and promotes a poverty mentality.

As usual, Mr EE good post! Enjoy reading your content.

I need to offer a counter-commentary to your reader Donna’s point on “going back to work”. A couple things here.

- First, it highly depends on the industry in which you work. The reader cited the IT field, which I agree changes frequently to where an IT professional’s could become obsolete if they leave the field for a matter of years. In the healthcare industry, one is required to participate in continuing education to maintain licensure. This helps keep you up-to-date. Additionally, there is such demand for healthcare professionals, the vast majority of folks half good at what they do will always have job demand. For instance, according to the Bureau of Labor and Statistics (BLS), physical therapists are projected to be in shortage of 44% between 2014-2024 based on employment trends and industry needs. Do you think you could command a decent salary independent of your age in this scenario? I do

- Second, subject of age and likely reference to energy level for working a job was mentioned. I say to this, if someone on FIRE had to return to work, who says they would have to do it full time or for years and years. So, you have a bad fews months and need to work for 12 months to stockpile money or pay bills. Ok, no big deal. Could easily be done. Just because you’re in your 50s doesn’t mean you are unable to muster the energy to work. Most of us FIRE folks have some degree of passion (and energy) and would likely do just fine.

- Lastly - other hustles. I echo Mr. EE’s comment on working jobs (keep in mind, could be just part time doing something you love to where it doesn’t feel like a j-o-b). dissimilar to our previous occupations. Do this to make ends meet. Plus, a lot of FIRE folks are entrepreneurial and have many secondary income streams. They could always lean more on these vehicles, and ramp up income to support declines in other areas.

Dave,

First: agree

Second: agree

Lastly: agree

Thanks for reading and chiming in!